Annuities: Just Say No.

on November 29, 2021

with No Comments

You don’t need their product. You don’t even need to know why their specific product is bad. Just say no.

You don’t need their product. You don’t even need to know why their specific product is bad. Just say no.

Understanding the most powerful sales techniques doesn’t change the fact that they tend to work.

If you are one of those consumers for whom the word “annuity” is enough to make them tune out a sales presentation, congratulations! You have have probably correctly understood the real challenges these products face.

No. I thought we’d decided not to give them a first look.

Most financial planning articles about annuities pull their punches.

“Up until recently” annuities were a bad idea. They still are.

Charitable gift annuities get an “A” for marketing and an “F” for performance.

The entire selling point of the immediate fixed annuity is a lower return in exchange for a guarantee. But when analyzed, the purchase price is a loss from which you can never recover.

“Variable annuities are garbage. They have huge expenses; big fees if you try to bag out before a certain point; and massive tax problems compared to other ways you can invest. But that’s what you’ll probably be steered to by a commissioned insurance salesperson.”

Once you buy this product, you’re stuck. All structured settlement transfers must take place through a court order…

The returns offered by immediate fixed annuities aren’t as good as they sound. The sleight of hand in this case is the immediate loss of 100% of your principal. They are fixed for you to lose and the insurance company to win.

The returns offered by immediate fixed annuities aren’t as good as they sound. The slight of hand in this case is the immediate loss of 100% of your principal. They are fixed for you to lose and the insurance company to win.

Lottery tickets are also a good deal, if you win – otherwise it is just a tax on people who can’t do math.

Because you can’t change your mind, and you can’t spend your money ahead of time, the best use of an immediate fixed annuity is to protect you from yourself. Call me wild and crazy, but this is not the risk I am worried about.

The returns offered by immediate fixed annuities aren’t as good as they sound. The slight of hand in this case is the immediate loss of 100% of your principal. They are “fixed” for you to lose and the insurance company to win.

The 3.8% Net Investment Income Tax (NIIT) is a Medicare contribution tax on investment income.

The reason can be explained through a simple analogy about an interior decorator.

If you have received a projection from your company which included a lump sum offer that you were interested in taking, you may want to analyze it again.

Some investable assets in the name of the child can currently keep $2,300 of unearned income from the tax rate of the parents.

Being a fiduciary means more, regardless of what the Department of Labor might write in their press releases.

If you have this fringe employer or former employer benefit, I hope you are able to take advantage of making small Roth IRA contributions throughout your retirement.

You don’t need to know why an annuity is a bad deal to say no.

Given the purposeful complexity and limitations to structured products we suggest you avoid them.

This was part of an intentional anti-ad campaign that my mother instituted to inoculate her children against the power of Madison Avenue.

I recommend the NAPFA search tool and suggest you avoid the CFP Board’s search tool until they change how they do their searches.

Here are the most common elder scams and how to prevent them.

In Publication 590B, the IRS gives an example to demonstrate how Roth contribution basis works in a Roth IRA.

It is always a good time to be reminded that an immediate fixed annuity is not an investment; it is an insurance product. This 2015 article by David John Marotta is a methodical unraveling of annuities and a description of the far superior alternatives.

By decoupling your standard of living from the size of your income, you have taken the first step toward financial freedom.

The worst cause of employer stress is the fact that there exist many financial salespeople who offer plans which benefit themselves at excessive cost to the employer and their employees.

As part of the requirements, the SEC wrote passages which must be included verbatim in each relationship summary. Some of that required text are so-called conversation starter questions.

There are two critically important investment principles during retirement: 1) Stay calm and 2) Rebalance.

The selection of what products we purchase or avoid for clients is based solely on what we believe gives our clients the best chance to meet their goals.

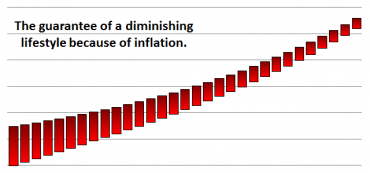

Setting aside some of the payment to cover future inflation is a prudent retirement planning practice.

When I was a teen, my grandfather George Marotta passed down to me his copy of “What You Need to Know Before You Invest” by Rod Davis. I recommend this book as way to gain a baseline understanding.

In addition to all of the other reasons people hate annuities, seemingly fraudulent advertising and sales techniques is a major factor.

As you read other financial advice sites, be wary of the sponsored content.

For investors who began working in 1970 and retired 45 years later in 2015, cash lost 83.83% of its purchasing power.

I couldn’t be prouder to be a NAPFA-Registered Financial Advisor.

Teresa Ghilarducci is just wrong here. There is no qualification that can make Ghilarducci more right.

Although this 1040 looks smaller, it is not an upgrade for anyone except for the IRS.

Our firm has become known for our method of computing maximum safe withdrawal rates in retirement. Our safe withdrawal rates are based on having what we believe to be optimum asset allocation targets.

In 2007 the Financial Planning Association won a lawsuit that it filed against the SEC to force them to enforce the registration provisions of the 1940 Investment Advisors Act. The law still isn’t enforced.

Albemarle Insurance Agency’s hiring solicitation shows the difference between insurance salesmen and fee-only fiduciary advisors.

Don’t let someone else live the life you’re saving for, but also don’t rely on Investor.Gov to protect your money.

Less gouging doesn’t make T-shares meet the high principles-based fiduciary standard.

Commission-based firms want either to be exempt from the Fiduciary standard or else given the title anyway.

The estate tax return is definitely complex, but that’s because it has to account for the multitude of special rules that only apply to a few households.

Here are the four criteria which must be met in order for margin loan interest to be tax deductible.

Any legislation which can include FINRA’s commission-based advisors will dilute what it means to be a fiduciary.