Fee-Only Is the Most Important Quality in Your Financial Planner

on September 1, 2023

with No Comments

The reason can be explained through a simple analogy about an interior decorator.

The reason can be explained through a simple analogy about an interior decorator.

We advocate for billing traditional IRAs to themselves but billing Roth IRAs to a taxable brokerage account. Here is the math of why.

One obscure way we bring value to clients is how we bill them.

If you weren’t spending your money on useless treatment, you could enrich your life in other ways, retire earlier, or be richer.

“It is, of course, hard to get people in any profession to do the right thing when they’re paid to do the wrong thing.”

Nice is different from good. You want a good financial planner not just a nice one.

“Has the focus on expense ratios caused the public to lose focus of more critical financial measures, such as performance?” Actually, expense ratios and 12b-1 fees should get even more attention than they are getting. Here’s why.

For the proper Victorian, acts of love and money should not mix. Although this honest conversion may ruffle Victorian sensibilities, it is a foundation of the trust we forge with our clients.

Excellence and low cost can go together.

You deserve advice from a firm where you don’t have to second guess where their loyalties lie.

It is relatively easy for fee-only fiduciaries to answer the question “How much do you charge?” The only fee they collect is the fee that the client directly pays them.

Incentives matter. If you are going to get a financial advisor, you need to select a fee-only advisor because you need to find an advisor you can trust.

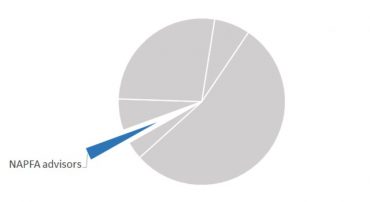

We were surprised by our survey of the registered firms in the Charlottesville area.

One obscure way we earn our fee is in how we bill you.

Investment managers can bring clients greater savings by carefully considering how they bill different types of accounts.

It should be clear that “fee-only” means “fee-only,” not “fees and third-party manager revenue-sharing and trailing mutual fund fees.”

Most investors are not aware of an important separation in the professionals of the financial services industry.

How your advisor is compensated matters. Make sure you can follow the money and know how they are getting paid.

Many will mislead you into thinking they are “fee-only” when they are not.

Inverview with George Marotta on NAPFA and being a fee-only fiduciary

Many people prefer having a local fee-only commission-free financial planner they can easily visit on a regular basis. Others prefer to handle everything through phone and email.

Fee-only financial planners are registered investment advisors with a fiduciary responsibility to act in their clients’ best interest. They do not accept any fees or compensation based on product sales.

Working with a fee-only planner can help you make better financial decisions and balance current needs with future goals. The result can be financial peace of mind.

“If you want advice that’s free of such conflicts, you’ll need to look for a true fee-only (not fee-based) financial planner.”