#TBT Are Democrats Or Republicans Better For The Stock Market?

on October 17, 2024

with No Comments

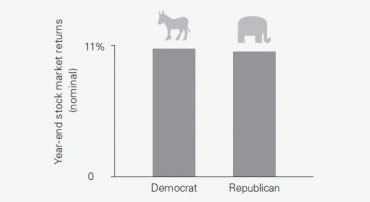

This 2017 article reminds us, “Stock market returns have little to do with which party holds the White House.”