At all times and at any age, you can withdraw as much as you have contributed to your Roth IRA without tax or penalty. Unfortunately, keeping track of how much you have contributed is complicated. First, there is no convenient place to keep track of regular Roth IRA contributions. Instead, you need to maintain your own records. Second, there are many different ways that assets can be added to a Roth IRA and each one adjusts your Roth contribution basis slightly differently.

At all times and at any age, you can withdraw as much as you have contributed to your Roth IRA without tax or penalty. Unfortunately, keeping track of how much you have contributed is complicated. First, there is no convenient place to keep track of regular Roth IRA contributions. Instead, you need to maintain your own records. Second, there are many different ways that assets can be added to a Roth IRA and each one adjusts your Roth contribution basis slightly differently.

In this series, I am reviewing each type of contribution one at a time and explaining how much counts as Roth contribution basis and when. This article is putting some of the pieces together by explaining step-by-step an example the IRS gives in Publication 590B.

In Publication 590B, the IRS gives an example to demonstrate how Roth contribution basis works in a Roth IRA. That example is:

Example.

Ishmael, age 32, opened a Roth IRA in 2000. He made the following transactions into his Roth IRA.

- In 2005, he converted $10,000 from his traditional IRA into his Roth IRA. He filled out a 2005 Form 8606 and attached it with his 2005 Form 1040. He entered $0 on line 17 of Form 8606 because he took a deduction for all the contributions to the traditional IRA; therefore, he has no basis. He entered $10,000 on line 18 of Form 8606. He also entered zero on Form 1040, line 15a, and $10,000 on line 15b.

- In 2016, he rolled over the balance of his qualified retirement plan, $20,000, into a Roth IRA when he changed jobs. He used a 2016 Form 1040 to file his taxes. He entered $20,000 on line 16a of Form 1040 because that was the amount reported in box 1 of his 2016 Form 1099-R. Box 5 of his 2016 Form 1099-R reported $0 since he didn’t make any after-tax contributions to the qualified retirement plan. He entered $20,000 on line 16b of Form 1040 since that is the taxable amount that was rolled over in 2016.

The total balance in his Roth IRA as of January 1, 2020, was $105,000 ($50,000 in contributions from 2000 through 2019 + $10,000 from the 2005 conversion + $20,000 from the 2016 rollover + $25,000 from earnings). He hasn’t taken any early distribution from his Roth IRA before 2020. In 2020, he made a contribution of $5,500 to his Roth IRA.

In August of 2020, he took a $85,500 early distribution from his Roth IRA to use as a down payment on the purchase of his first home. See his filled out Illustrated Recapture Amount—Allocation Chart to see how he allocated the amounts from the above transactions. Based on his allocation, he would enter $20,000 on his 2020 Form 5329, line 1 (see Amount to include on Form 5329, line 1, earlier). He should also report $10,000 on his 2020 Form 5329, line 2, and enter exception 09 because that amount isn’t subject to the 10% additional tax on early distributions.

From 2000-2019, Ishmael contributed $50,000. The precise years of these contributions does not matter as regular contributions are always available for tax-free withdrawal, but the example tells us his Roth IRA was opened in 2000. For that to happen, he needed to have funded it for at least $1, so I have assume that he contributed $2,500 per year for each of those 20 years.

In 2005, he did a Roth conversion of $10,000 from a traditional IRA with no nondeductible basis.

In 2016, he did a Roth conversion rollover of a traditional qualified plan such as a traditional 401(k) plan of which the full $20,000 was taxable.

In 2020, he contributed $5,500 more, making his total regular Roth contributions $55,500.

Also in 2020, he distributed $85,500. From the $85,500, $0 was taxable according to Form 8606 Line 25c, but $10,000 was subject to the 10% early withdrawal penalty. Here’s how that math worked out.

Below is a timeline of what Ishmael is assumed to have done:

| Years Ago | Year | Amount | Action | Regular Contributions | Rollover Contributions | Reported On… |

|---|---|---|---|---|---|---|

| 20 | 2000 | $2,500 | contribution | $2,500 | $0 | |

| 19 | 2001 | $2,500 | contribution | $2,500 | $0 | |

| 18 | 2002 | $2,500 | contribution | $2,500 | $0 | |

| 17 | 2003 | $2,500 | contribution | $2,500 | $0 | |

| 16 | 2004 | $2,500 | contribution | $2,500 | $0 | |

| 15 | 2005 | $10,000 | converted from traditional IRA | $0 | $10,000 | 2005 Form 8606, line 17. Nondeductible basis: $0 18. Taxable amount of conversion: $10,000 |

| 15 | 2005 | $2,500 | contribution | $2,500 | $0 | |

| 14 | 2006 | $2,500 | contribution | $2,500 | $0 | |

| 13 | 2007 | $2,500 | contribution | $2,500 | $0 | |

| 12 | 2008 | $2,500 | contribution | $2,500 | $0 | |

| 11 | 2009 | $2,500 | contribution | $2,500 | $0 | |

| 10 | 2010 | $2,500 | contribution | $2,500 | $0 | |

| 9 | 2011 | $2,500 | contribution | $2,500 | $0 | |

| 8 | 2012 | $2,500 | contribution | $2,500 | $0 | |

| 7 | 2013 | $2,500 | contribution | $2,500 | $0 | |

| 6 | 2014 | $2,500 | contribution | $2,500 | $0 | |

| 5 | 2015 | $2,500 | contribution | $2,500 | $0 | |

| 4 | 2016 | $2,500 | contribution | $2,500 | $0 | |

| 4 | 2016 | $20,000 | Roth conversion rollover from qualified plan | $0 | $20,000 | 2016 Form 1040, line 16 a. Pension and Annuities: $20,000 b. Taxable Amount: $20,000 |

| 3 | 2017 | $2,500 | contribution | $2,500 | $0 | |

| 2 | 2018 | $2,500 | contribution | $2,500 | $0 | |

| 1 | 2019 | $2,500 | contribution | $2,500 | $0 | |

| 0 | 2020 | $5,500 | contribution | $5,500 | $0 | |

| Total | $55,500 | $30,000 |

Then, Ishmael withdraws $85,500 from his Roth IRA.

If you withdraw sufficient money from your Roth IRA that you are withdrawing from your rollover contribution basis (money sourced from Roth conversions), then a portion of your withdrawals may be considered what the IRS calls a recapture amount.

The idea is that if you were to have withdrawn early directly from your traditional IRA, you would have been faced with a 10% early withdrawal penalty. Without the recapture amount, doing a Roth conversion and then withdrawing from your Roth IRA would mean that you avoid this penalty. To make it so that taxpayers can’t use such a simple loophole to avoid the penalty, the IRS says that if it has been less than five years since you converted, then you still have to pay the 10% penalty when you withdraw from that rollover contribution basis.

Said another way: If you withdraw $10,000 from your traditional IRA when you are age 40, you would owe a 10% tax on the distribution. If you convert that $10,000 to Roth IRA and then distribute, the IRS doesn’t want you to be able to get out of the 10% penalty. As a result, they make you include Roth conversions younger than 5 years old as a “recapture amount” penalized on Form 5329 even though it is from a rollover contribution basis.

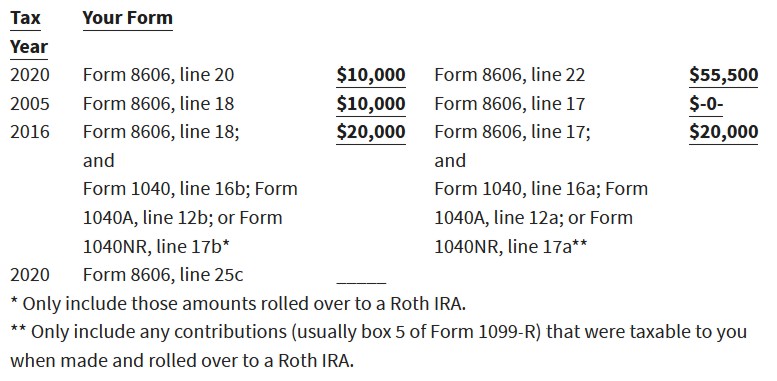

The IRS tells us that Ishmael uses the allocation chart as follows to calculate his recapture amount:

This chart shows us that in order to withdraw the full $85,500, Ishmael needs to withdraw some from his Roth conversion rollover contribution basis.

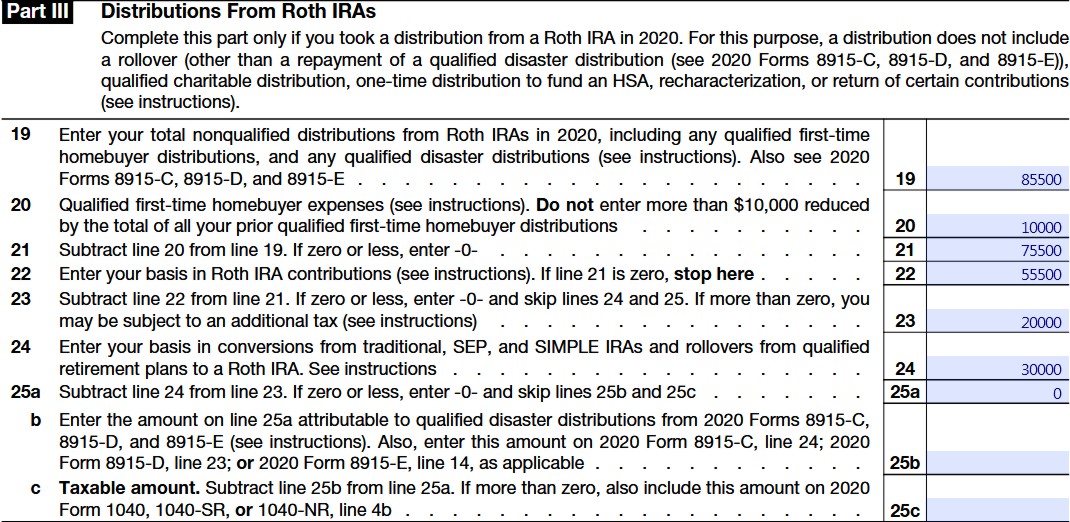

You can see from this chart that his Form 8606 line 25c is blank. While they don’t tell us how Ishmael fills out his Form 8606 Part III, presumably he has filled it out like this:

All of his distributions are non-qualified because, even though his Roth IRA has been open at least five years, Ishmael does not meet one of the other requirements of over age 59 1/2, dead, or disabled.

He is using his qualified first time homebuyer expense lifetime limit on Line 20. Then, he enters his regular Roth contribution basis ($55,500) on line 22 and his rollover contribution basis ($30,000) on line 24.

Line 25c is $0 because he has withdrawn only up to his contribution and conversion basis total in his Roth IRA. This is why no portion of his withdrawal is included in taxable income.

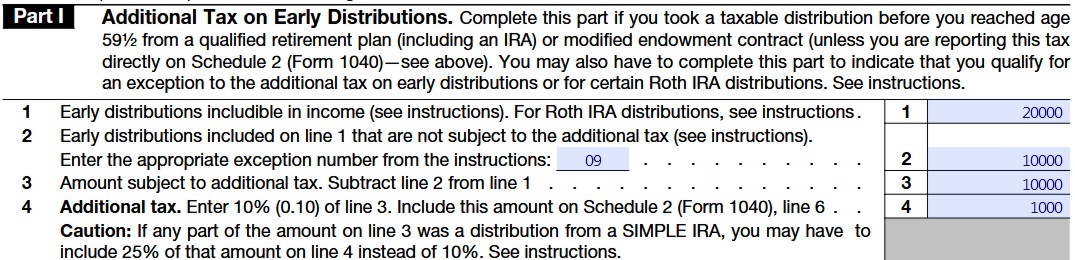

Because the 2016 Roth conversion is only 4 years old when he withdrew from it, it needs to be included as a recapture amount on Form 5329.

The instructions for Form 5329 Line 1 say:

If you received an early distribution from your Roth IRAs, include on line 1 the part of the distribution that you must include in your income. You will find this amount on line 25c of your 2020 Form 8606. You will also need to include on line 1 the following amounts.

- A qualified first-time homebuyer distribution from line 20 of your 2020 Form 8606. Also include this amount on line 2 and enter exception number 09.

- Recapture amounts attributable to any conversions or rollovers to your Roth IRAs in 2016 through 2020. See “Recapture amount subject to the additional tax on early distributions” next.

Because he withdrew from his 2016 conversion / rollover basis, he needs to include that total as a recapture amount on Form 5329 line 1. This makes his Form 5329 as follows:

You can see that he needs to report $20,000 of the withdrawals on Form 5329 line 1 “Early distributions includible in income” and $10,000 on line 2 “Early distributions included on line 1 that are not subject to the additional tax.” While this second $10,000 number matches his 2005 Roth conversion amount, it is actually the $10,000 of his qualified first-time homebuyer expense.

The first-time homebuyer expense is exempt from the 10% penalty.

While Ishmael’s withdrawal of his young Roth conversion is not taxable as income, it is subject to the 10% penalty as a recapture amount.

The Roth conversion rollover contribution basis is available for tax-free withdrawal right away, but if the conversion is too young and you do not meet a different exception to the penalty, your distribution will face the 10% early distribution penalty.

If Ishmael had waited a year and withdrawn in 2021, his Roth conversion would have been five years old and he would have had no recapture amount or early distribution penalty.

If Ishmael had been older at age 60 instead of 32, then he would have been older than age 59 1/2 and his distribution would not have been an early distribution and thus have no penalty or tax.

The Roth withdrawal rules are more complicated than they first appear, but funding your Roth IRA still remains one of the best financial decisions you can make.

Photo by Linda Söndergaard on Unsplash

Latest posts from Megan Russell

- Four DPOA Limitations at Schwab and Their Solutions - July 23, 2024

- #TBT Implement the Automatic Millionaire at Schwab - July 18, 2024

- How to Implement a DPOA at Schwab - July 16, 2024