From December 2016 through July 2017, CFA Institute published a five post series called “Where Markets Fail” by Jason Voss. In the posts, Voss set out to “point out some of the often hidden, unrecognized, ignored, or forgotten assumptions underlying the functioning of markets in capitalism.”

From December 2016 through July 2017, CFA Institute published a five post series called “Where Markets Fail” by Jason Voss. In the posts, Voss set out to “point out some of the often hidden, unrecognized, ignored, or forgotten assumptions underlying the functioning of markets in capitalism.”

The series is very political in nature, but, perhaps because it was published at CFA Institute, Voss tries to stay away from the political side. In the comments, he tries very hard to say that he is pointing out the weak points of the market without suggesting that anything should be different. In other words, he may be talking about “the price preeminent” and, yes, that does sound like a central planning concept, but he is not trying to argue for central planning.

Fair enough. Although his fixation on “the right price” points out some of his own prejudices and qualms with the “free” part of “free market.”

In his replies to the comments on his series, Voss is very polite but often a bit vague. He writes a lot of emotionally charged sentences lacking clarity. I am not surprised he feels so misunderstood and has to repeat himself a lot.

In a thread with one commenter on his first post , Voss replies:

To be an active manager requires that you disagree with the market price, presumably, to borrow your term, because you are “a more intelligent person.” If you believe markets are perfect discounting mechanisms, then there is no advantage to buying anything but the market. That is the strong-form of the efficient market hypothesis. It sounds like you reject that thinking, yet you defend free-markets as perfect discounting mechanisms. To me, this is not institutional rivalry, as it goes to the heart of whether you believe markets are perfect or not. I do not think they are perfect; which is what I am going to continue to demonstrate in the next four articles, too. Again, my motivation is to help analysts and investors to do a better job.

I believe strongly in the efficient market hypothesis. The efficient market hypothesis suggests that individual stocks are correctly priced by the market until new information becomes public, moving stock prices so they are again correctly priced. When something unexpected occurs, the market responds to and incorporates the new information faster than any one intelligent person could.

Index investing or passive investing seeks to track the return of a portion of the market. The opposite is active management, which seeks to beat the return of the markets by using market timing and individual stock selection. If an investment manager believes the markets are inefficient to some degree, that manager will err on the side of active management because they will believe that they know better than the markets some times.

However, I think that active management compared to index investing is like a gambler compared to the gambling house. Although one person may be able to best the house in one game during one time period, the house is going to best the gambler across the whole floor of games over the long haul. The superior returns of active management are the product either of luck (legal but not repeatable over the long haul) or of trading on insider information (often illegal).

Ironically, active managers do worse than the market on average. On average, there are as many actively-managed funds underperforming its index as outperforming its index, because there are active managers on each side of any given trade. Then, with their higher than normal fees and expenses, they cannot as a group do better than index investing.

Many active managers do beat the market during any given time period just as some pennies repeatedly come up heads. And since every active manager believes that they are smarter than average those lucky ones whose pennies repeatedly come up heads will attribute their success to their own genius. Statistically, though, the number of successful active managers is no greater than you would expect luck to generate given the number of active managers.

Perhaps the best way to explain the difference between active management and our methodology of portfolio constructions is that our investment philosophy is not dependent on finding the lucky fund manager who will beat the S&P 500 during the next decade. We look at the characteristics of each sector of the markets over long periods of time and invest in that track record. At no point are we entrusting reaching our goals to the ability of a fund manager to pick stocks and time the markets.

Given a dozen stellar financial planning firms, only one will have the best returns over any five or ten year period. Yet given the right methodology, every firm could help clients ensure that they have the best chance to meet their goals and secure a safe and prosperous retirement.

The political views of your investment manager matter for this reason. An investment manager who is “at times a soft socialist” like Voss will be more likely to engage in active management, market timing, and gambling on individual stocks because they believe a central planner like themselves can know better than the free markets. They will also, on average, charge more because they believe that their genius is worth it.

In contrast, an investment manager who leans libertarian will be more likely to engage in methodical portfolio construction, index investing, and a diversified asset allocation because they believe in the efficiency of freedom, including the free markets. They will also, on average, have lower fees and expenses.

Voss himself was an active manager before being a so-called “content director” at CFA. His website biography says:

Over the course of his investment career as co-Portfolio Manager of the Davis Appreciation & Income Fund (DAIF) the fund bested the NASDAQ by 77.0%, the S&P 500 by 49.1% and the DJIA by 35.9%.* The DAIF was regularly ranked in the top decile of its investment category and further it earned a Lipper #1 ranking. The Fund was named a Lipper Leader, and was a perennial Morningstar Analyst Pick . Most impressively, the DAIF was one of Morningstar’s first ten mutual funds given a Stewardship Grade of “A.”

The footnote admits that his career was a 5-year time frame:

* Results include the effects of dividends and stock splits on total return. Results were calculated based on data published by Yahoo! Finance; DAIF ticker symbol is DCSYX and covering the period of September 22, 2000 to August 18, 2005 – the length of Jason Apollo Voss’ tenure as co-portfolio manager of the Davis Appreciation & Income Fund.

The Davis Appreciation & Income Fund (DCSYX) is a Balanced Fund currently invested with just 70.55% in stocks. Comparing the return of DCSYX during the bursting of the technology bubble to all-stock indexes such as the technology laden NASDAQ, or large cap S&P 500 and DJIA is not a fair comparison. DCSYX it is also currently invested with 3% in Mid-Cap Value and 5% in Mid-Cap Blend. Mid-Cap did much better during this time period than large cap or growth indexes. Boasting about DCSYX’s returns by comparing its returns to the returns of the NASDAQ, S&P 500 or DJIA violates basic benchmarking principles the CFA Institute teaches.

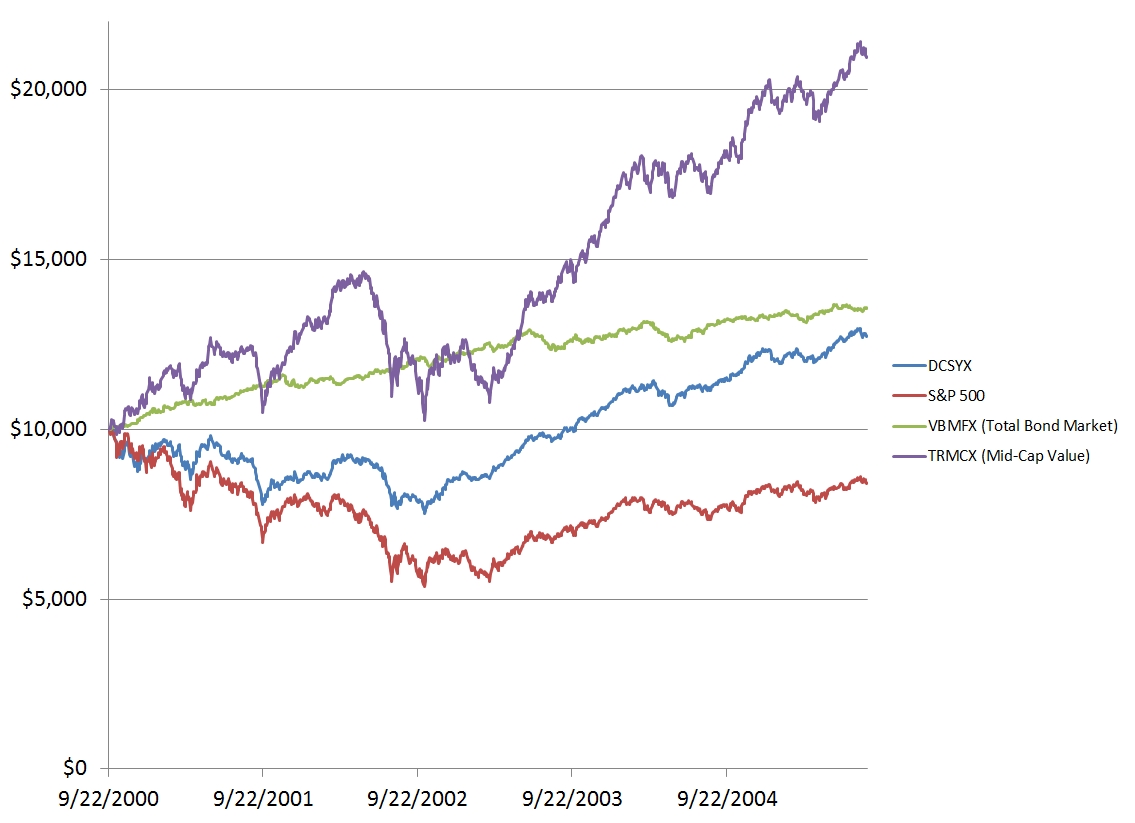

At right is a graph of the growth of $10,000 in DCSYX over that time period charted against the S&P 500, T. Rowe Price Mid-Cap Value (TRMCX), and Vanguard Total Bond Market Index Fund Admiral Shares (VBTLX). Although we don’t know what the mix of DCSYX was during the time period in question, here are those assets charted against each other during that time period. You can see Mid-Cap Value (purple) did the best, followed by the Total Bond Market (green), then DCSYX (blue), trailed by the S&P 500 (red).

At right is a graph of the growth of $10,000 in DCSYX over that time period charted against the S&P 500, T. Rowe Price Mid-Cap Value (TRMCX), and Vanguard Total Bond Market Index Fund Admiral Shares (VBTLX). Although we don’t know what the mix of DCSYX was during the time period in question, here are those assets charted against each other during that time period. You can see Mid-Cap Value (purple) did the best, followed by the Total Bond Market (green), then DCSYX (blue), trailed by the S&P 500 (red).

Even if we could compare DCSYX to an appropriately blended portfolio, the results wouldn’t be very meaningful. Five years is too short a time period to determine anything.

It is a mistake to select, review, or judge a fund based on recent or short-term returns. In order to get meaningful statistics, you need to use the longest time horizon possible. Even 30 years is not long enough to judge which investment will have a higher mean return for the next 30 years. For example, we recently had a 30-year time period where long term bond returns beat the return for stocks even though when you look at longer time periods stocks beat bonds.

Even if you grant some “moderate predictive power” to the various ratings, rankings, and stars, lower expense ratios are better at predicting future returns.

Morningstar Stars are based on a fund’s 1-, 3-, 5-, and 10-year returns, but even 10 years is not long enough to determine a fund’s statistically superior performance. And while mutual funds and their managers will continue to tout their high ratings and rankings, you should ignore them. Every commission-based mutual fund salesman knows how to build a portfolio of six mutual funds all with an excellent 5-year track record from their company’s family of funds. Having more stars and a good 5-year track record increases sales, but it has little to do with your chance of meeting your goals.

You deserve a custom asset allocation made with your specific goals in mind. You deserve diligent contrarian rebalancing. You deserve a fiduciary standard of care. You deserve a financial advisor that passionately believes in the free market.

Read the whole series of articles responding to the series “When Markets Fail” by Jason Voss here:

Part 5: The Markets Fail to Remove Risk

Fraud is the enemy of the free markets. It is theft through deception.

Part 4: The Markets Fail the Utopian Vision

The markets may fail the Utopian Vision, but only because our Tragic world fails the Utopian Vision.

Part 3: The Markets Fail People Who Price Their Goods Too Low

Pricing is not about being nice. It is about being fair. Fair to you as the seller and to the value you ascribe to the good or service.

Part 2: The Markets Fail a Moral Standard

Private property, free markets, and protection from aggression solve a lot of problems.

Part 1: The Markets Fail Centralized Planning

The free market fails to be a centralized economy. That’s why it is called “free.”

Photo by Raw Pixel on Unsplash

Latest posts from Megan Russell

- Four DPOA Limitations at Schwab and Their Solutions - July 23, 2024

- #TBT Implement the Automatic Millionaire at Schwab - July 18, 2024

- How to Implement a DPOA at Schwab - July 16, 2024

Latest posts from David John Marotta

- #TBT A Review of Finances at Age 60 - July 25, 2024

- #TBT Implement the Automatic Millionaire at Schwab - July 18, 2024

- #TBT Stress Is Not Your Enemy - June 27, 2024