Taxes on Non-Deductible IRA Contributions

on June 20, 2014

with No Comments

“Once you put cream in the coffee, all coffee removed from the cup is partly cream and partly coffee.”

“Once you put cream in the coffee, all coffee removed from the cup is partly cream and partly coffee.”

Roth accounts have several advantages over traditional retirement accounts.

How to report a backdoor Roth in Turbo Tax.

A complete guide to using Roth IRAs to build lasting wealth.

Many people lack the time and expertise to develop an intelligent retirement asset allocation plan.

We have created several asset allocation tools to aid those seeking an intelligently diversified portfolio.

A backdoor Roth IRA contribution requires some extra steps but allows high-income earners equal access to the tax-free benefits of a Roth IRA.

A dollar saved on your taxes is better than a dollar earned which causes you to pay more tax.

As the payroll processor at our company, how quickly do I need to deposit 401(k) contributions into employee accounts? -Sincerely, Payroll Pam

Money deducted from your paycheck for retirement typically gets deposited quickly into your 401(k) plan. But this isn’t always the case.

Mr. Roth can also help with transferring gifts to your heirs, setting up your first emergency reserve account, and paying for a new house or college expenses. But don’t ask him to iron your clothes. That’s where he draws a line.

Tax-free saving for retirement is only one of the many talents offered by Mr. Roth. If you have yet to become fully acquainted, consider this your formal introduction and start getting to know Mr. Roth today.

President’s proposal comes with silver linings for shrewd advisors

$3 million today has the same buying power as $500,000 in 1970.

If you look beyond the short term, making this move is pretty clearly worse than using a high-interest credit card to pay your bills.

You should have no problem naming your nephew as your beneficiary, but accessing the money from India after your death is more complicated.

These kittens have retirement plans. Be more like these kittens.

Literally tens of thousands of employees who were once participants in an employer-sponsored retirement plan (i.e., 401(k) plan, profit-sharing plan) neglect to take their retirement money with them.

Following the holiday season, many will feel the effects of overindulging on festive sweets. It turns out that your 401(k) also suffers when indulging on too much of a good thing.

There is a backdoor way to contribute to a Roth IRA for those who are not income eligible. This method requires the following steps:

This article reviews the coordination rules which govern the maximum contributions to 457, 401(k) and Thrift Savings Plan. Information on 403(b) plan maximums is also included.

It’s time to consider adjusting your retirement savings. The Internal Revenue Service recently issued a variety of inflation adjustments for 2013, and retirement savers can now save even more.

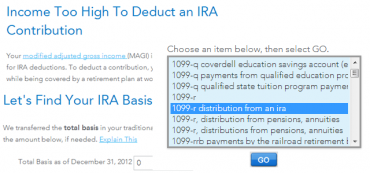

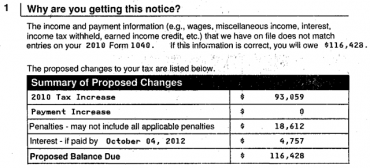

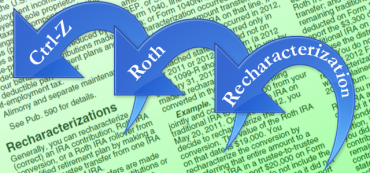

Currently the IRS is sending notices to anyone who did a Roth Recharacterization in 2010 asking them to pay as though they kept the entire conversion amount.

There is a separate set of rules for those under age 55 or who are looking to distribute from an IRA. These rules focus on an exception called Substantially Equal Periodic Payments (SEPPs).

Here are three questions that every small business owner should answer before establishing a new retirement plan.

Precious metals will, on average, just keep up with inflation, but your after tax return would mean you fell behind inflation by the 28% tax you must pay.

Here is the only question you should attempt to answer: Are you paying a higher tax rate now or later?

Should it be invested aggressively, like 100% equities, or use the same split as my taxable investments, such as 50-50 stocks vs bonds?

“How can you respond if these new taxes are enacted? One option is to do a Roth conversion so that you can pay taxes now for those retirement funds.”

Nearly everyone is an excellent candidate for a Roth conversion this year. You can always undo part or all of a Roth conversion with what’s called a recharacterization, so you can’t convert too much.

Who would have thought that someone earning $10,700 might want to purposefully push their taxable income up to $217,450 this year in order to pay $47,595 more in taxes at these lower 2012 tax rates?

Who would have thought that someone in the 33% tax bracket now who will be in a lower 28% tax bracket in the future might want to do a Roth conversion at his higher rates now?

Who would have thought that someone earning $400,000 might want to purposefully push their taxable income up to $1.2M this year in order to pay $280,000 more in taxes at these lower 2012 tax rates?

Who would have thought that someone earning $75,000 might want to purposefully push their taxable income up to $275,000 this year in order to pay as much as possible at these lower 2012 tax rates!

Nearly everyone is an excellent candidate for executing a Roth conversion this year. But it is helpful to have a target amount in mind before you begin.

A Roth provides more flexibility than its Roth 401(k) counterpart because you can access the principal at any time without penalty.

A tax tsunami is coming at the end of this year. This will be your last opportunity to safeguard your assets in a lifeboat and avoid getting swamped with taxes.

Q: I am a 65-year-old retired widow and I have a large IRA. How should I invest if I don’t need this money?

Q:What advice can you offer for how to go about accessing retirement funds after a hardship?

I’m in my 20s and I’m just getting started in the working world. I’m also looking at a Roth IRA. Is there a certain Roth you recommend?

I’m in my 20s and I’m just getting started in the working world. Which of the attached 401(k) investment choices do you recommend?

David John Marotta was featured in a Wall Street Journal article about the upcoming Roth recharacterization deadline.

Marotta’s Roth segregation technique of conversion and recharacterization was featured in InvestmentNews magazine.

Between threats of cutting tax benefits and crackdowns on non-compliant plans, for the retirement industry ‘stakes are higher than they ever were’

If the GAO were giving you investment advice they would suggest that you not participate in your 401(k) and convert at least half of your retirement savings into an annuity laden with fees and expenses.

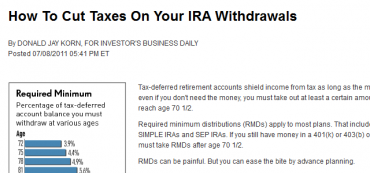

This article from Donald Jay Korn for Investor’s Business Daily describes the benefits of advance tax planning to reduce the tax bite that is inevitable as you grow older and required minimum distributions (RMDs) become a larger portion of your retirement account.

David Marotta discusses how to maximize retirement accounts.

Most plans have funds laden with fees. Some share this revenue with plan sponsors, enticing them to pick more expensive funds to subsidize the costs of the plan or even make a profit.

An individual 401(k) (also known as a “solo 401(k)”) offers you the option to defer the first $16,500 of income.

With the income tax debate currently controlled by legislators advocating even higher rates, I don’t think you will regret having some tax free money.