Tax Efficient Investing

on June 29, 2012

with No Comments

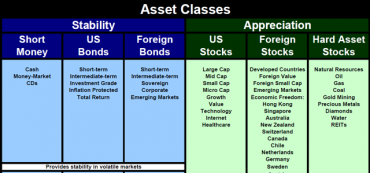

It can be useful to maintain a grid where all of the available asset classes are arranged in order, by tax efficiency and potential return based on time horizon, so clients can clearly see when and where tax-deferral can offer the greatest benefits.