The University of Virginia offers a 403(b) Tax Deferred Savings Plan (TDSP) available through Fidelity Investments. There are two sides to the account: one is a Traditional account which takes pretax contributions, the other is a Roth account which takes post-tax contributions. For most families, contributing to the Roth account is preferable.

In 2016, you are allowed to contribute up to $18,000 to your 403(b). If you are age 50 or older, you are allowed to contribute an additional $6,000 for a total of $24,000. These limits are separate from your Roth IRA limits, meaning you can both contribute the maximum to your Roth IRA and your Roth 403(b).

For most families, they should fund their Roth accounts even if they are just converting their savings to Roth or feel they can’t afford it.

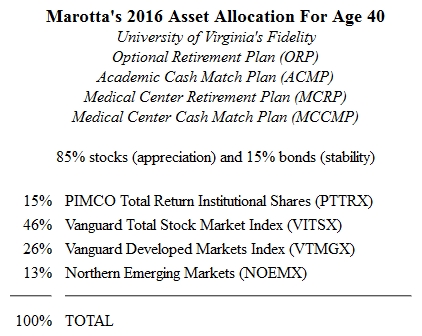

In addition to 403(b) plans, the University of Virginia also offers a series of 401(a) plans including the Optional Retirement Plan (ORP), Academic Cash Match Plan (ACMP), Medical Center Retirement Plan (MCRP), and Medical Center Cash Match Plan (MCCMP). The selection of investment choices for the Fidelity 401(a) plans are all the same, and they are less extensive than the 403(b) plan.

With all of these choices and more outside of UVA, we recommend reading our article “Which Retirement Account Should I Fund?” to help prioritize your funding. But in general, your priority should be to take advantage of any employer match, then fund all your Roth accounts, then consider traditional tax deferred, and finally taxable savings. You can remember this priority by remembering our name as the acronym – Ma.Ro.T.Ta: Match, Roth, Traditional, and Taxable.

Comprehensive wealth management is much more than just an asset allocation, but an asset allocation is a good place to start. We have created asset allocation models from the UVA Fidelity 403(b) and 401(a) choices available.

The 401(a) plans have a smaller number of choices. You can use our UVA Fidelity 401(a) Plans Calculator to create your age-specific asset allocation, but for the purposes of demonstration this is the asset allocation we recommend for a typical 40-year old.

We used PIMCO Total Return Institutional Shares (PTTRX) with an expense ratio of 0.46% simply because it is a good fund and had the lowest expense ratio among the bond choices. PTTRX has the highest expense ratio for any of the funds we are recommending. Some of the choices we rejected have expense ratios as high as 2.26%. Studies by Morningstar suggest that low fees and expenses are a better predictor of future returns than Morningstar stars.

We are always trying to reduce the cost of the funds we select in order to keep more of the gains for the investor. In today’s market, we believe that brilliant asset allocations can be built for total portfolio expense ratios that are less than 0.25%

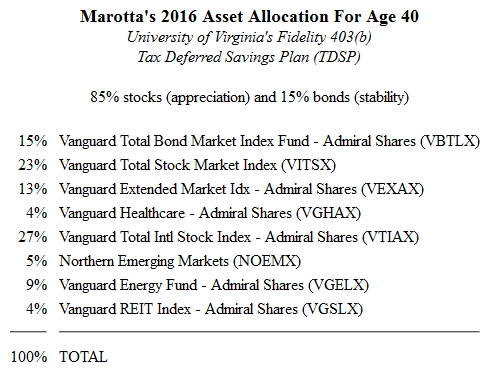

The Fidelity 403(b) had better bond choices, including our selection: the Vanguard Total Bond Market Index Fund Admiral Shares (VBTLX) with an expense ratio of 0.07%.

For the U.S. stock allocation in the 401(a), we decided to use the Vanguard Total Stock Market Index (VITSX) with an expense ratio of just 0.04%. This fund follows a cap weighted index which includes all U.S. stocks.

Normally we recommend tilting small and value in order to boost returns. We opted against adding any additional funds because the only small cap value fund had an expense ratio of 0.81% and because current pricing suggests that a dynamic asset allocation should not favor this tilt.

We used the same fund (VITSX) for the 403(b) U.S. allocation but we also added Vanguard Extended Market Idx – Admiral Shares (VEXAX) with an expense ratio of 0.10%. VEXAX cheaply adds extra weight to the mid and small cap style boxes. We considered adding Vanguard Small Cap Value Index Investor Shares (VISVX) with an expense ratio of 0.23%, but decided against it because of the higher than necessary expense and the current indicators for a different tilt.

From the 403(b) options, we also added a small allocation to Vanguard Healthcare – Admiral Shares (VGHAX) with an expense ratio of 0.29%. In general, we recommend overweighting both technology and healthcare, but the technology fund choices had expense ratios of 0.74% or higher.

For the 401(a) foreign stock allocation, we split the allocation two thirds in Vanguard Developed Markets Index (VTMGX) with an expense ratio of 0.09% and one third in Northern Emerging Markets (NOEMX) with an expense ratio of 0.34%. This technique of putting one third in the option with a higher expected return and a higher volatility usually finds a nice blend of risk and return for long periods of time.

For the 403(b) foreign stock selection, we were able to lower the average expense ratio and still get a similar mix. We used Vanguard Total Intl Stock Index – Admiral Shares (VTIAX) with an expense ratio of 0.14% in place of VTMGX. VTIAX includes not only developed countries but it also includes the emerging markets and Canada. Since VTIAX includes 17.1% emerging markets a smaller portion can be put into NOEMX, the emerging market fund with a higher expense ratio.

Our sample 401(a) portfolio for a typical 40-year old has an expense ratio of just 0.15%. By comparison, the Vanguard Target Date Retirement Funds available in the plans have expense ratios around 0.18%. We don’t normally recommend target date funds. Their underlying mix varies widely from company to company even when they have the same target date. Furthermore, target date funds often have higher than necessary expense ratios.

We believe Vanguard target date funds are too conservative. Normally, our typical 40-year old would have a retirement target date of 2041, when they turn 65. But to achieve a close-to-correct asset allocation, you would have to look at the target date for someone 10 years younger or 2050. We prefer using our suggested mix with more emerging markets as well as a lower overall expense ratio.

For the 403(b) portfolio, we included two allocations to resource stock funds which were not available among the 401(a) choices. Resource stocks dropped precipitously last year which contrarians know means it is time to rebalance and invest more. The first fund is the Vanguard Energy Fund – Admiral Shares (VGELX) with an expense ratio of 0.31% and the second is Vanguard REIT Index – Admiral Shares (VGSLX) with an expense ratio of 0.12%.

Despite the recent drop in the price of resource stocks, long term studies suggest that an allocation to these categories should boost returns by more than the added expense ratios of these funds.

Here is the resulting 403(b) portfolio for a typical 40-year old:

Fees matter and these choices are some of the best for balancing diversification with lower expenses. Lower fund choices make the average expense ratio for the 403(b) portfolio just 0.13%.

Crafting an asset allocation for a retirement plan with limited choices is the art of determining if the added expense is worth the expected return for each potential asset class. We often wish that retirement plans would include both more options and the lower costs options we use in our own 401(k) plans.

That being said, the University of Virginia plan includes funds sufficient to produce these excellent portfolios.

Photo used here under Flickr Creative Commons.

Latest posts from David John Marotta

- How To Distribute from A College America 529 Plan to an Account Owner - October 22, 2024

- #TBT Are Democrats Or Republicans Better For The Stock Market? - October 17, 2024

- How To Distribute from A College America 529 Plan to a Designated Beneficiary - October 15, 2024

Latest posts from Megan Russell

- #TBT Don’t Increase Your Bond Allocation In Bear Markets - October 24, 2024

- How To Distribute from A College America 529 Plan to an Account Owner - October 22, 2024

- How To Distribute from A College America 529 Plan to a Designated Beneficiary - October 15, 2024