I’ve heard it said that asset allocation means always having something to complain about. A brilliant asset allocation will have long periods when one or more component of the portfolio fails to appreciate. And for investment management a long period of time can be a decade or more.

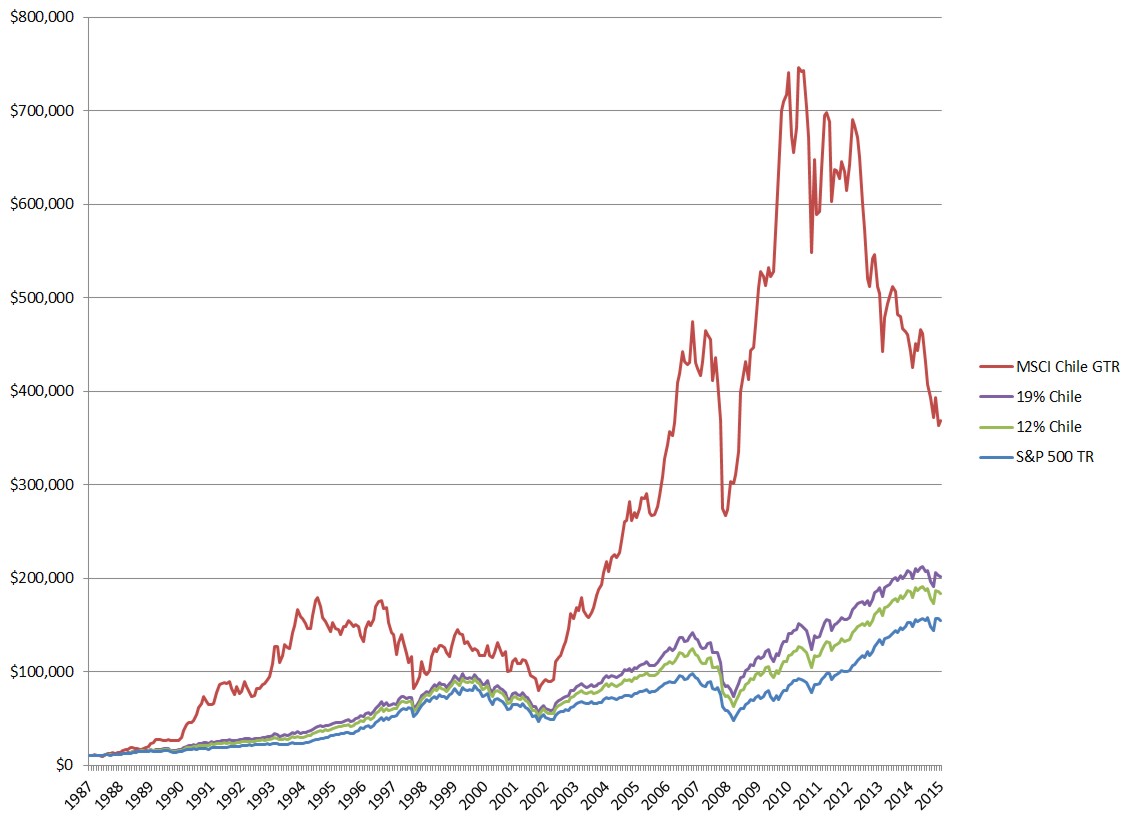

This past year the MSCI Chile Gross Index lost -16.58% as measured in US dollars. Chile is down -50.64% since it peaked at the end of April, 2011 with a 5-year annual return of -13.04%.

The longer the downturn for a particular portfolio holding the greater the feeling that we should simply eliminate it from the portfolio. It is “doing nothing but going down” we say because our minds are apt to frame the movement in the present tense rather than the past tense. Our brains are very quick to find short term patterns and project them forward as long term trends.

This cognitive ability is useful in many areas, but it is not particularly useful in investment management.

Investments are inherently volatile. The rebalancing bonus which comes from having an asset allocation is dependent on two variables: volatility and correlation. The more volatile and less correlated your asset classes are the greater the rebalancing bonus you get from having those components in your portfolio.

When you compare Chile to the S&P 500 Total Return since the beginning of 1988 when the Chile Index began, the S&P 500 had a 1,540.25% appreciation, growing $10,000 into $154,669. It averaged 10.28% annually.

Even though the S&P 500 had phenomenal growth during the time period, it also experienced an entire decade where it dropped -29.48% and a 30 month period where it dropped -43.75%.

Over the same time period, Chile had a 3,585.25% appreciation, growing $10,000 into $368,524. It averaged 13.75% annually.

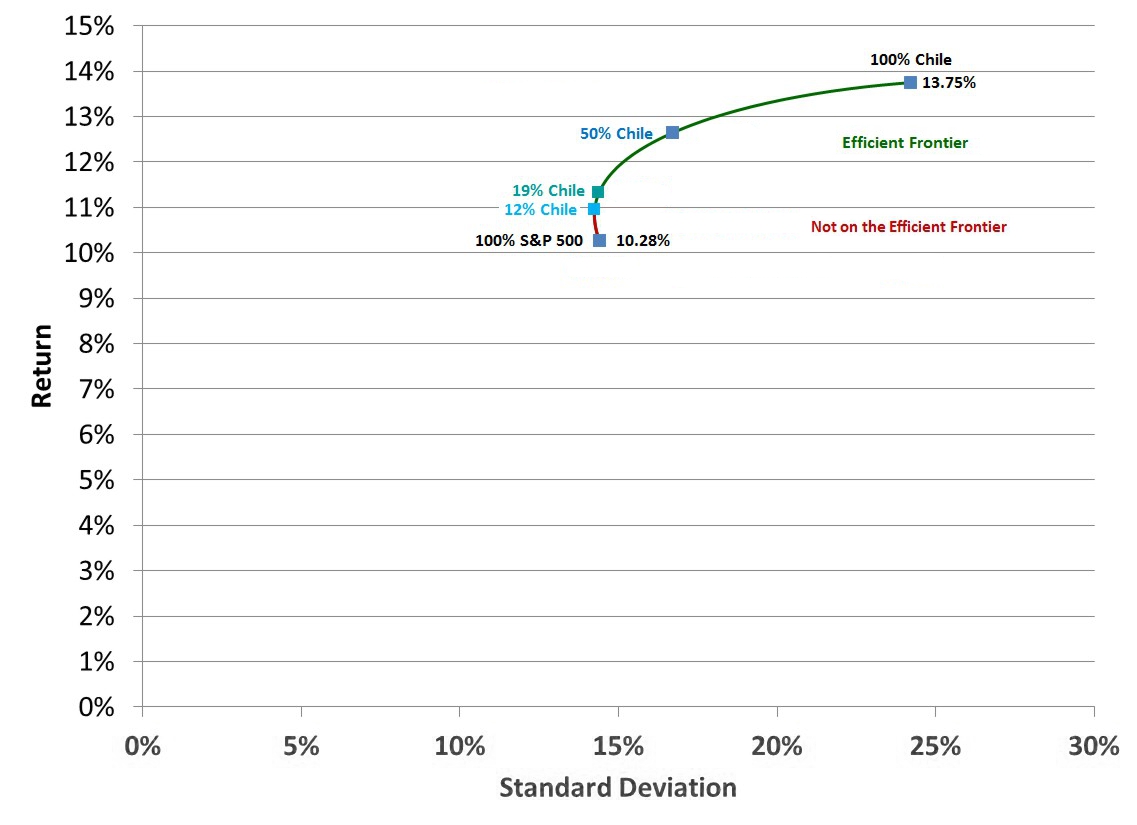

Having twice as much growth as the S&P 500 over 28 years comes with the price of greater volatility. The standard deviation of annual returns for the S&P 500 was 14.39% while the standard deviation for Chile was 24.21%.

This type of volatility is normal for the markets. While you might have had more money putting everything in Chile, we recommend a blended portfolio. Each individual component of a balanced portfolio is more volatile than the portfolio as a whole. Thus, adding a little bit of Chile to your portfolio can boost returns and reduce volatility on account of the rebalancing bonus.

In fact, over this time period the mix which had the lowest volatility was 12% Chile and 88% S&P 500. This blended portfolio had an average return of 10.96% and a standard deviation of just 14.25%. This is a boost to annual returns of 0.68%. Over this time period, adding 12% Chile to your portfolio resulted in an extra $29,095 over the S&P 500 alone.

Creating a mix of 19% Chile and 81% S&P 500 would have had no more volatility than a portfolio of 100% S&P 500. But this portfolio would have averaged 11.32%, an extra 1.05% annually and earned an additional $46,784.

The return of these blended portfolios over long periods of time produce a risk return curve which can help investors find what asset allocation produced the greatest return for a given amount of risk. These blended portfolios are called the efficient frontier and produce curves between moving from 100% S&P 500 to 100% Chile.

Notice that with only these two choices, investing any less than 12% in Chile is not on the efficient frontier because there is a portfolio for which a greater return could have been achieved while experiencing an equal or lower volatility.

In actual portfolio construction, there are dozens of components which are being fit together to craft a brilliant investment strategy for long term time horizons. Our current asset allocation model usually invests less than 2% of a portfolio’s value in Chile. Even if Chile were to lose half of its value the portfolio value would only go down 1%. Assuming that Chile doesn’t move in sync with other investments in the portfolio, this is a level of volatility which is acceptable for the potential additional return.

As it turns out, the correlation between the monthly returns of Chile and the S&P 500 are low at 0.46.

It is always disappointing when an investment category fails to perform as hoped. But after an investment has fallen in price it is often that much more attractive looking forward.

Unlike individual stocks, a country index cannot go to zero. If the Chile index approached zero, you would be able to take your pocket change and buy every publically traded company in Chile. Long before you could do that, people much wealthier than you would notice how low the price was and they would buy every company in Chile. Low prices for a country index is best thought of as the index going on sale.

Stocks often move on very light trading as a few sellers push the stock price lower. Market makers who hold all the stocks in the index gradually move the price lower when there are more sellers than buyers. A market maker is forced to buy when there is no one else interested in buying. But at some point the price is low enough to wake up other potential buyers and the movement in price finds resistance. This can cause greater swings of volatility often over long periods of time.

As a result, you should not be afraid of an major index. Assuming there were good reasons to be invested in it in the first place, a 3, 5 or even 10 year down turn is not a reason to abandon your brilliant investment strategy.

Latest posts from David John Marotta

- How To Distribute from A College America 529 Plan to an Account Owner - October 22, 2024

- #TBT Are Democrats Or Republicans Better For The Stock Market? - October 17, 2024

- How To Distribute from A College America 529 Plan to a Designated Beneficiary - October 15, 2024

Latest posts from Megan Russell

- How To Distribute from A College America 529 Plan to an Account Owner - October 22, 2024

- How To Distribute from A College America 529 Plan to a Designated Beneficiary - October 15, 2024

- #TBT Vote Early Instead of Voting Absentee (Virginia) - October 3, 2024