Successful tax planners understand the value of Roth savings. A short-sighted or simplistic approach to Roth conversions could lead to having less after-tax net worth over the long-term.

Successful tax planners understand the value of Roth savings. A short-sighted or simplistic approach to Roth conversions could lead to having less after-tax net worth over the long-term.

In our first article in this series, we showed how paying the tax on your Roth conversion is actually one of the benefits, sheltering more assets in qualified retirement accounts.

In the second article, we demonstrated how reducing your required minimum distributions (RMDs) and retaining more IRA assets is another benefit of Roth conversions.

In this article, we are looking at how Roth conversions can decrease your taxable income and increase your tax savings over the long haul.

During retirement, the government employs five distinct tax rates.

Taxes on Ordinary Income

The first tax is the ordinary income tax rate. This is the standard tax rate that most people know and talk about.

Currently in 2024, the ordinary income tax rates are 10%, 12% 22%, 24%, 32%, 35%, and 37%. However, absence an act of Congress, these rates will increase in 2026.

Ordinary income is any taxable income which is not qualified. Roth conversions are one example of ordinary income.

Most financial writers writing about Roth conversions mistakenly only look at ordinary income tax brackets. However, the other tax rates are also important to Roth conversion analysis, as you will see.

Taxes on Qualified Income

The second tax is the qualified income tax rate. This tax primarily applies to qualified dividends and capital gains. Currently in 2024, the main qualified income tax rates are 0%, 15%, and 20%. Each qualified income tax rate is less than the corresponding ordinary income rate. This is why qualified income is viewed as tax-advantaged.

While Roth conversions and IRA distributions are not taxed at qualified rates, the size of your taxable IRA distributions will affect the size of your qualified income tax rate.

Ordinary Income, even though not taxed in the qualified brackets, helps to determine which qualified rate will be applied.

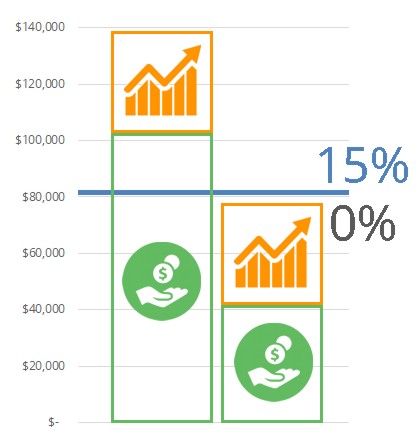

At right, you can see a simple diagram showing this point. The orange qualified income of each of these two individuals is identical. However, the size of their green ordinary income puts them in different qualified tax brackets. Because the first person makes over $100,000 of ordinary income, their first dollar of qualified income is taxed at the 15% rate and they do not have any non-taxable qualified income. The second person has less ordinary income and is able to have none of their qualified income taxed as a result.

Roth conversion targets should keep these qualified rates in mind both in the year of conversion and in later years when IRA withdrawals might occur.

In our example at right, imagine that one year of required minimum distributions is the difference between the first taxpayer and the second. By doing a Roth conversion earlier in her life, the second person is able to realize capital gains during retirement free of taxation.

In this way, Roth conversions today can lower taxable income in the future, potentially saving money on qualified taxation.

Taxes on Investment Income

The third tax is the net investment income tax or NIIT. This tax imposes 3.8% of further taxation on so-called investment income when a taxpayer has an MAGI of over $200,000 single or $250,000 married.

These thresholds are not inflation adjusted. This means that over time more people with lower gross incomes will face this additional taxation.

It also means that you can potentially avoid this taxation entirely if you reduce your taxable income over time. If you have a traditional IRA, the only way to reduce your taxable income in the long-run is to have smaller required minimum distributions in the future through either large Roth conversions or IRA withdrawals today.

IRA withdrawals larger than you need produces excess taxation in your taxable brokerage account, as shown in our second article of this series. However, larger Roth conversions are effective at reducing future taxable income.

Taxes on Social Security

The fourth tax is the phaseout of nontaxable Social Security. As your income increases, a larger portion of your Social Security benefits becomes taxable.

Social Security income over $32,000 married ($25,000 single) has 50% of the benefit taxable, and Social Security income over $44,000 married ($34,000 single) has 85% of the benefit taxable. These thresholds are not inflation adjusted. This means that over time more people with lower incomes will face this additional taxation.

Non-taxable Social Security is excluded from AGI, while taxable Social Security is included in AGI. This means that in addition to subjecting more income to taxation, taxable Social Security also increases your chances of being exposed to other AGI-based taxes.

Imagine a taxpayer whose provisional income (half of Social Security plus all other adjusted gross income) is exactly the second threshold. Currently, they are likely in the 12% income tax bracket. However, for every $100 of new ordinary income not sourced from Social Security, $85 more of their Social Security benefits would be taxed as well. This is an effective tax of 22.2%, even though the taxpayer is nominally in the 12% top marginal bracket.

This excess effective tax rate continues until the cap on taxable Social Security is reached and 85% of all Social Security benefits are taxed.

These examples of a higher than expected tax rate followed by a lower rate again are called “tax torpedoes.” Avoiding these tax torpedoes is one of the benefits of systematic Roth conversion strategies.

Taxes on Health Insurance

Fifth and finally, healthcare costs are now modified adjusted gross income (MAGI) dependent.

Before Medicare, the premium tax credit (the Affordable Care Act’s health insurance subsidy) is phased out for those on marketplace plans as household income surpasses various multipliers of the poverty line.

When on Medicare, a Medicare premium surcharge known as an Income Related Monthly Adjustment Amount (IRMAA) is imposed on seniors with a higher MAGI.

Medicare IRMAAs are thousands of dollars for the year and are imposed for even $1 over the threshold. In this case, the marginal tax rate is nearly infinite.

Systematic Roth conversions are one method to reduce the cost of Medicare premiums. Doing a Roth conversion for one year might result in lowering your MAGI in many subsequent years by lowering your required minimum or taxable IRA distributions.

Concluding Thoughts

The value of doing systematic Roth conversions is often much higher than people expect. None of these tax effects are accounted for with simplistic advice regarding Roth conversions. It requires complex long-term personalized tax planning to compute this effect.

Our tax team models everything we know about a specific client’s situation, and then approximates doing their taxes in mock every year until they reach age 100. After modeling this baseline, we then try various scenarios and compare the client’s after-tax net worth in each case to their baseline after-tax net worth. Only after doing somewhere around a hundred of these scenarios can you estimate how much the optimum Roth conversion might be worth.

By keeping your income low in retirement, you can avoid unnecessary Medicare IRMAAs as well as qualified income, investment, and Social Security taxation.

There is a lot of tax savings available for those who can make it into the lowest tax brackets. The potential for that future tax savings can sometimes justify massive Roth conversions before retirement.

Photo by Iryna Ogarkova on Unsplash. Image has been cropped.

Latest posts from David John Marotta

- How To Distribute from A College America 529 Plan to an Account Owner - October 22, 2024

- #TBT Are Democrats Or Republicans Better For The Stock Market? - October 17, 2024

- How To Distribute from A College America 529 Plan to a Designated Beneficiary - October 15, 2024

Latest posts from Megan Russell

- #TBT Don’t Increase Your Bond Allocation In Bear Markets - October 24, 2024

- How To Distribute from A College America 529 Plan to an Account Owner - October 22, 2024

- How To Distribute from A College America 529 Plan to a Designated Beneficiary - October 15, 2024