Over a year ago I suggested that you avoid these eight broker-dealers based solely on the principle that they petitioned the CFP Board to delay enhancing their own fiduciary standard until the Securities and Exchange Commission (SEC) brought out their own rules:

Over a year ago I suggested that you avoid these eight broker-dealers based solely on the principle that they petitioned the CFP Board to delay enhancing their own fiduciary standard until the Securities and Exchange Commission (SEC) brought out their own rules:

- Ameriprise Financial Services Inc.

- Morgan Stanley Wealth Management

- LPL Financial

- RBC Wealth Management US

- Wells Fargo Advisors

- Edward Jones

- UBS Financial Services Inc.

- AXA Advisors

We would recommend avoiding these firms based solely on their attempt to delay the CFP Board’s fiduciary standard alone. But there are many other reasons consumers might want to avoid these firms, not the least of which is how they make their money.

Since writing that article the SEC did finally release “Regulation Best Interest,” a terrible regulation that falls far short of a fiduciary standard and does more harm than good. I am glad that the CFP Board rejected and ignored the delaying and diluting strategy of these commission-based financial sales companies.

Also since writing my original article, I have published articles illustrating why Ameriprise pay-to-play funds are poorly ranked by Morningstar and that they were fined $5.4M for brokers stealing client funds, as well as why you should beware sloppy retirement advice from firms like Wells Fargo Asset Management.

Now from the UBS Group comes a story of how they overcharged and misled wealthy clients for a decade without detection .

The Hong Kong Securities and Futures Commission said client advisers and assistants at the Swiss bank regularly added extra fees and padded out spreads on bond and structured-note trades, taking “profits from its clients without agreement with or disclosure to them.” Around 5,000 clients overpaid on about 28,700 transactions, it said. …

The overcharges came in the form of extra fees that went beyond contractual caps on charges, and in the bank scooping up the gain when client trades went through at better prices. In some cases, UBS staff falsified quarterly statements to financial intermediaries to conceal the excess charges, the SFC said.

The regulator said the bank failed to act in clients’ best interest in the trades for around seven years, then took two more years to report the misconduct after finding it. …

“The SFC considers that these malpractices involved a combination of serious systemic failures for a prolonged period of time including inadequate policies, procedures and systems controls, lack of staff training and supervision, and failures of the first and second lines of defense functions at UBS,” it said.

Consumers often presume that an advisor associated with a large commission-based brokerage firm will have a team of managers supervising their advisor. This is a misconception.

UBS has a market capitalization of $64.5 billion. I don’t know why some consumers say they “feel more comfortable with a large firm,” but apparently many do. As of the end of last year, UBS Financial Services (CRD# 8174) had $496 billion in assets.

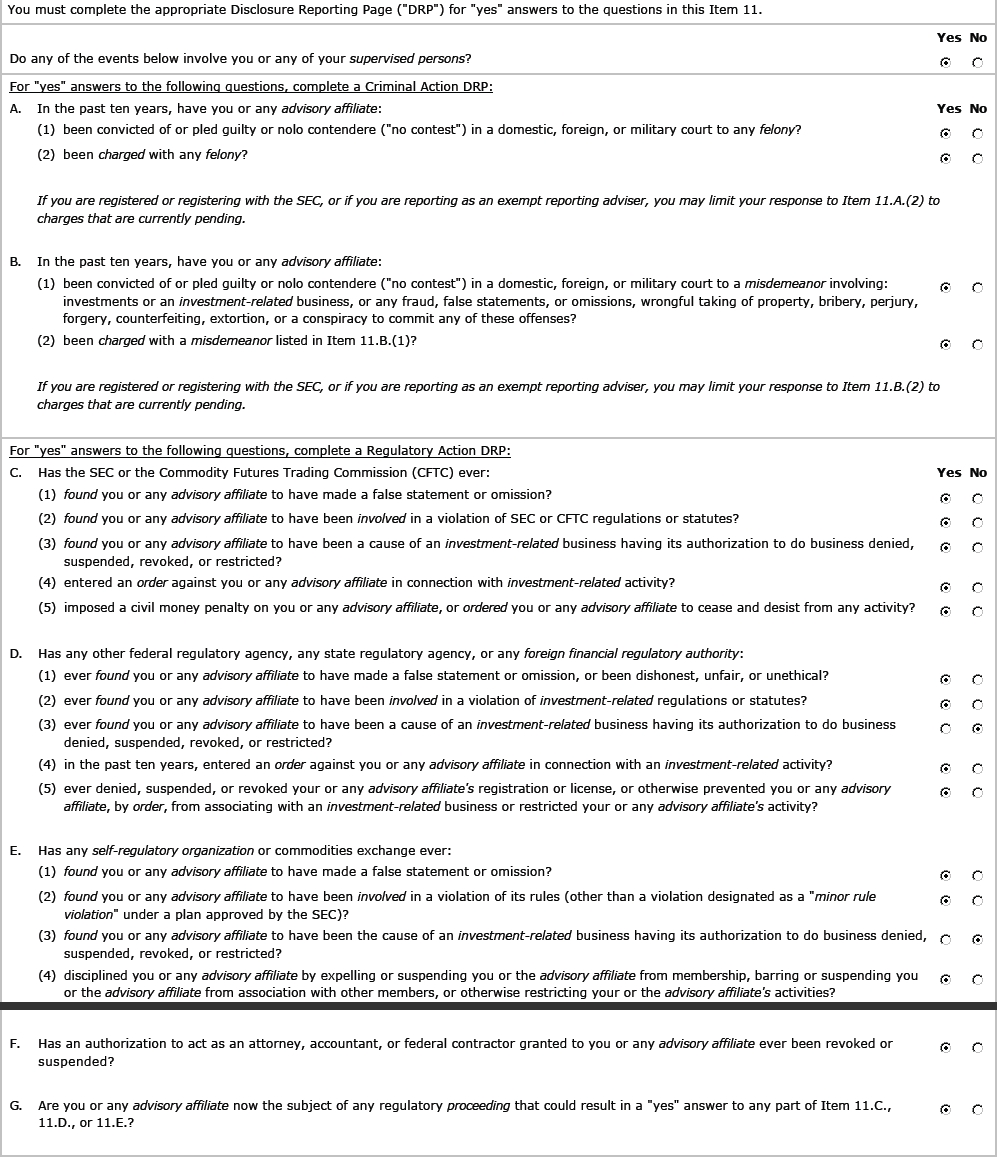

Meanwhile UBS has a regulatory disclosure with the SEC that they “have been convicted or pled guilty or no contest to felonies”, “have made false statements or omissions”, “have been in violation of SEC or CFTC regulations or statues”, etc. The list of types of Disclosure Reporting Pages is bad enough, but the number of Criminal Action Disclosure Reporting Pages is even worse. A separate Disclosure Reporting Page is required for each event or proceeding and the disclosures begin on page 174, continuing for over a thousand pages through page 1,232.

At large firms, compliance is often done by a team of lawyers at corporate headquarters, while the individual advisor may have no more compliance, ethics training, or oversight than whatever seminar attendance is required every two years.

One of the most common United States Securities and Exchange Commission violations found at large firms is failure to provide adequate supervision and monitoring of what their commission-based advisors were doing, often in order to generate the largest possible commissions. Incentives matter. With the wrong incentives in place, it can be difficult for even well-intentioned advisors to overcome the subconscious temptation to rationalize their actions.

In UBS Financial’s ADV Part 2 , they claim to offer “fee-based Financial Services,” a description that the CFP Board has suggested is misleading.

They also describe the many ways they get paid explaining in part (emphasis part of original document):

Compensation to Financial Advisors Who Recommend Advisory Programs

In general, we pay our Financial Advisors cash compensation consisting of two components: a guaranteed monthly minimum draw required by applicable law, and production payout if it exceeds the monthly minimum draw. The production payout is a percentage (called a payout or grid rate) of the product-related revenue (called production) that each Financial Advisor generates during that month with respect to the clients he or she serves, minus certain adjustments that are specified by our Financial Advisor Compensation Plan.The payout rate or grid rate is generally based on production levels and ranges from 28% to 50%. Financial Advisors working as part of a team that meets minimum production requirements can qualify for a higher grid rate (but not above 50%) than they would receive working as an individual.

We reserve the right, at our discretion and without prior notice, to change the method by which we compensate our Financial Advisors and employees, including reducing and/or denying production payout and/or awards at our discretion for any reason.

We believe you should avoid any advisor who is paid a commission based on the production of product-related revenue to his or her firm.

UBS’s ADV Part 2 also says that their “financial planning services do not make investment recommendations” nor do they “analyze or assess the investment merits of particular securities or investments.”

They also make it clear that “it is your responsibility to determine if, and how, the suggestions made in connection with the Financial Planning Services should be implemented or otherwise followed.” They continue to warn that you (and not they) should consider “all relevant factors in making these decisions” by consulting with a tax professional or estate planning attorney before you implement a particular strategy.

Prior to financial planning, your only choice was to deal with financial product salesmen. Now that financial planning has been around for more than 50 years, we believe you deserve better than a commission-based advisor like you might get at UBS.

Today consumers have choices, including the choice to select a fee-only fiduciary advisor who offers comprehensive, integrated, and personal financial planning.

Photo by sutirta budiman on Unsplash

Latest posts from David John Marotta

- #TBT A Review of Finances at Age 60 - July 25, 2024

- #TBT Implement the Automatic Millionaire at Schwab - July 18, 2024

- #TBT Stress Is Not Your Enemy - June 27, 2024