Our firm uses an asset allocation approach to portfolio construction. This is supported by a belief that a balanced asset allocation will over time reduce volatility and boost returns through regular, programmatic rebalancing. We allocate a portion of our managed portfolios to foreign stocks, and within it we prioritize the countries highest in economic freedom, according to the Heritage Foundation’s Index of Economic Freedom. Hong Kong is the highest ranked country on the latest edition of the index and has one of the largest country-specific allocations in our portfolios.

Hong Kong is a small nation (462 square miles) composed of a peninsula and a collection of islands along the South China Sea and is completely surrounded by China. It is home to 7.3 million people clustered into an area approximately six times the size of Washington, D.C. The country is a financial hub both for traditional banking and property holding companies as a result of it’s attractive regulatory environment. Hong Kong’s economy has largely transformed into a post-Industrial arrangement and it will continue to evolve as the 2047 expiration of the “one country, two systems” agreement with China approaches.

Hong Kong’s stocks are tracked through the MSCI Hong Kong Index, composed of the large- and mid-cap portions of the investable market. The index is composed of 44 holdings primarily within the Financials sector (61%), with some exposure to Utilities (13%) and Industrials (15%).

Our firm uses the iShares MSCI Hong Kong Index ETF (EWH) to invest in Hong Kong’s stock market. The ETF has an expense ratio of 0.48%, which is lower than the 0.69% category average for ETFs in this sector.

The fund’s top holdings (as of 8/1/2016) are:

| 1 | AIA Group Limited | 18.24% |

| 2 | CK Hutchison Holdings Ltd | 8.32% |

| 3 | Hong Kong Exchanges & Clearing Ltd. | 6.72% |

| 4 | Sun Hung Kai Properties Limited | 4.88% |

| 5 | Cheung Kong Property Holdings Limited | 4.55% |

| 6 | CLP Holdings Limited | 4.03% |

| 7 | Link Real Estate Investment Trust | 3.92% |

| 8 | Jardine Matheson Holdings Limited | 3.52% |

| 9 | Hong Kong & China Gas Co. Ltd. | 3.49% |

| 10 | Hang Seng Bank, Limited | 3.21% |

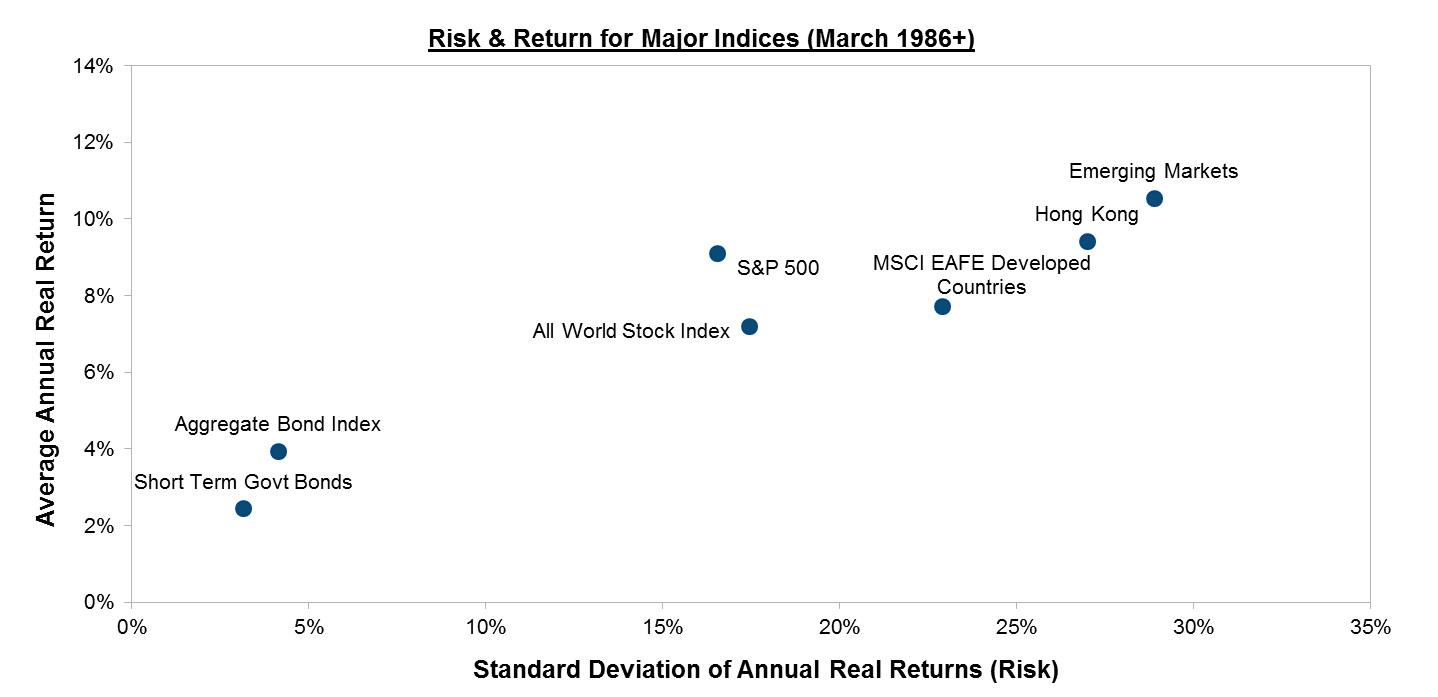

Hong Kong has a different risk-return profile from most major indices. Its risk and return are both nearly at the mid-point between the Developed Foreign Stocks (represented by the MSCI EAFE Developed Countries Index, of which Hong Kong is a part) and Emerging Markets.

Investors seeking to boost returns to a portfolio with Developed Foreign stocks could simply add Emerging Markets exposure, but they could also add Hong Kong. Historically, we’ve historically advocated for including an allocation to Emerging Markets but portfolios have benefited from inclusion of Hong Kong as well because of the diversification it provides in a regularly-rebalanced portfolio.

Rebalancing can boost a portfolio’s returns or lower its volatility. The bonus from rebalancing increases when holdings have a lower correlation or a higher volatility. Correlation is a measurement of how frequently two assets move in sync with each other. Hong Kong has a 59% correlation with the MSCI EAFE Developed Countries index, which means the assets move out of sync with one another nearly as often as they move in sync.

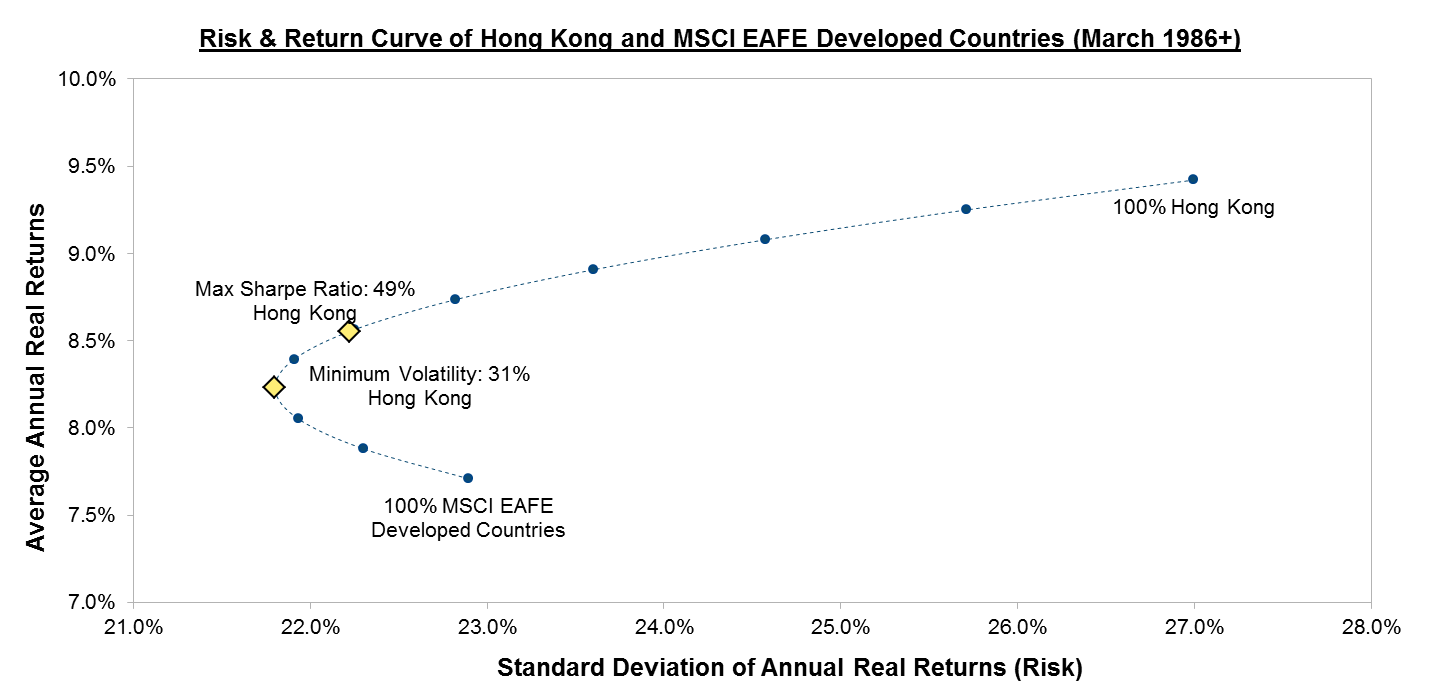

Building a portfolio of assets that don’t move in sync with one another means you can construct a portfolio of assets stronger than the sum of the parts. You can visualize this by plotting the overall risk and return of many different “portfolios” composed of the EAFE Developed Markets Index and Hong Kong. Simply adding Hong Kong into the portfolio’s mix both reduces risk and increases return. If investors sought to generate the most efficient foreign stock portfolio from these two assets portfolio–generating the maximum return per unit risk taken–then they would have been served best by allocating 49% to Hong Kong and 51% to the EAFE Index.

| MSCI EAFE Developed Countries | Hong Kong | Max Sharpe Ratio | Minimum Volatility | |

| Return | 7.77% | 9.42% | 8.55% | 8.23% |

| Risk | 22.90% | 27.00% | 22.22% | 21.80% |

| Sharpe Ratio* | 0.34 | 0.35 | 0.38 | 0.38 |

| Hong Kong (%) | 0% | 100% | 49% | 31% |

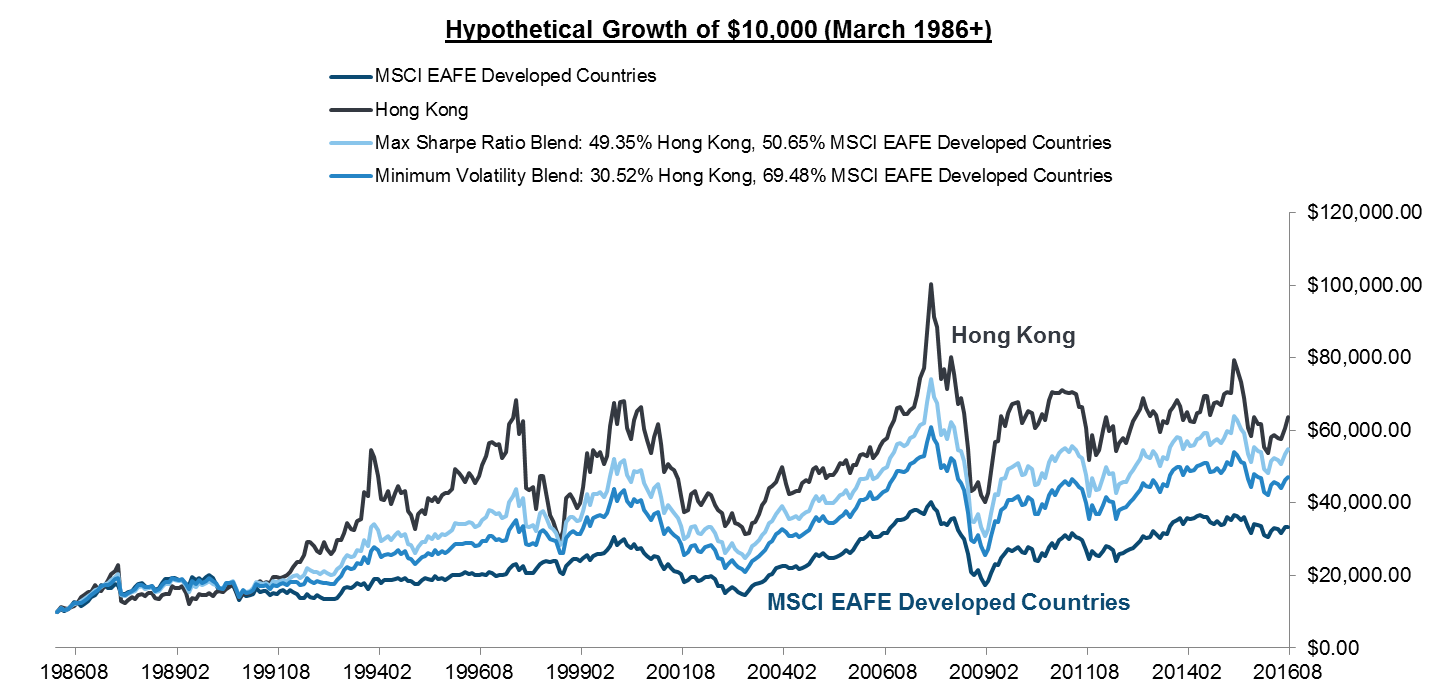

Hong Kong presents investors with many routes to improve a portfolio, or to boost returns within an allocation to foreign stocks. Since April 1985, Hong Kong’s returns have been more volatile than Foreign Stocks as a whole, but it also delivered a greater return. The additional return more than makes up for the risk, but a mix is better than either of the two individual assets. Investors seeking to minimize volatility should have historically supplemented Foreign Stocks with a 31% allocation to Hong Kong, which would have also boosted returns. We’ve written before about the risk-minimizing impacts of diversification, and adding Hong Kong to a foreign stock allocation has simultaneously boosted returns and lowered risk. Investors seeking the most efficient portfolio judged on the basis of return-generated-per-amount-of-risk-taken (referred to as the Sharpe Ratio) should have also included an allocation to Hong Kong because it more than justifies its riskiness with additional return. The “most efficient” mix between Foreign Stocks and Hong Kong, historically, was actually 51% Hong Kong.

Portfolio construction is at its core a science and an art. A careful investor measures the risk and return of the multitude of available assets and crafts a portfolio meant to have the greatest chance of success going forward. It’s relatively simple to construct the portfolio that would have performed best. Our investment process acknowledges that we cannot know what the future holds. Instead of predicting the future, we use the risk and return profiles of many assets with limited correlation to one another to construct portfolios that are greater than the sum of their parts.

Disclaimer: The authors and many clients of the authors own the funds mentioned in this article.

Notes: Past performance is not a guarantee of future returns. Top holdings information from ETF.com. Sector average expense ration from ETFDB.com. Foreign Stock index uses MSCI EAFE Index. Risk-free rate assumed to be 0% for Sharpe Ratio calculations. Minimum volatility and Maximum Sharpe Ratio portfolios based on proprietary analysis of past returns and volatility. Index data defined as follows: Short Term Bonds: Barclays 1-3 Year Government Index (1/1976+); Aggregate Bond Index: Putnam Income Fund A Shares (12/1954-12/1975), Barclays Intermediate Aggregate Bond Index (1/1976+); S&P 500: Ken French US sector data (7/1926-12/1969), S&P 500 Composite Total Return (1/1970+); All World Stock Index: MSCI All World Index (1/1988+); MSCI EAFE Developed Countries: MSCI EAFE Developed World Index (1/1970+); Emerging Markets: Average of MSCI EM Europe and Latin America indices (1/1988-12/1993), Lipper Emerging Markets Funds IX (1/1994-12/1998), MSCI Emerging Markets Index (1/1999+); Hong Kong: Hang Seng Equity Index (4/1985+); Real returns calculated based on CPI index.

Photo used here under Flickr Creative Commons.

Latest posts from David Loughin

- Healthcare Stocks And Asking “Relative To What?” - November 16, 2016

- The Case for Investing in Energy Companies - October 12, 2016

- Investing In Hong Kong Has Lowered Risk and Boosted Returns - September 28, 2016

Latest posts from David John Marotta

- #TBT A Review of Finances at Age 60 - July 25, 2024

- #TBT Implement the Automatic Millionaire at Schwab - July 18, 2024

- #TBT Stress Is Not Your Enemy - June 27, 2024