Portfolio construction eventually boils down to asking the question “relative to what?” and we overweight the Healthcare sector relative to the market capitalization-weighted US index of stocks. Why do our portfolios systematically overweight healthcare stocks? Healthcare and Technology are consistently among the best performing sectors in the US economy. We think these sectors are, not coincidentally, areas where United States companies continually lead the way. Investing because of a narrative thesis is a problematic way to construct a portfolio, so we are attracted to Healthcare because of its ability to boost returns, diversify a portfolio and reduce risk.

Portfolio construction eventually boils down to asking the question “relative to what?” and we overweight the Healthcare sector relative to the market capitalization-weighted US index of stocks. Why do our portfolios systematically overweight healthcare stocks? Healthcare and Technology are consistently among the best performing sectors in the US economy. We think these sectors are, not coincidentally, areas where United States companies continually lead the way. Investing because of a narrative thesis is a problematic way to construct a portfolio, so we are attracted to Healthcare because of its ability to boost returns, diversify a portfolio and reduce risk.

Our firm currently uses three primary funds for Healthcare exposure: Vanguard’s Healthcare ETF (VHT), the Vanguard Healthcare Fund (VGHAX), and the iShares Global Healthcare ETF (IXJ). iShares Global Healthcare (IXJ) and Vanguard Healthcare Fund (VGHAX) both include international Healthcare stocks while the Vanguard Healthcare ETF (VHT) is US-only. Otherwise, these funds differ only minimally and they each have minimal expense ratios.

Top 10 Holdings by Fund:

(As of 11/11/2016)

| Vanguard Healthcare ETF (VHT) | iShares Global Healthcare ETF (IXJ) | The Vanguard Healthcare Fund (VGHAX) | |

| 1 | Johnson & Johnson (10.15%) | Johnson & Johnson (8.08%) | UnitedHealth Group Inc. (6.47%) |

| 2 | Pfizer Inc. (6.52%) | Pfizer Inc. (5.19%) | Allergan plc (5.93%) |

| 3 | Merck & Co., Inc. (5.39%) | Novartis AG (5.03%) | Bristol-Myers Squibb Co. (5.69%) |

| 4 | UnitedHealth Group Incorporated (4%) | Merck & Co., Inc. (4.3%) | Merck & Co. Inc. (5.6%) |

| 5 | Amgen Inc. (3.96%) | Roche Holding Ltd Genusssch. (4.2%) | AstraZeneca plc (4.68%) |

| 6 | Medtronic Plc (3.78%) | UnitedHealth Group Incorporated (3.19%) | Eli Lilly & Co. (4.5%) |

| 7 | AbbVie, Inc. (3.21%) | Amgen Inc. (3.15%) | Medtronic plc (3.5%) |

| 8 | Gilead Sciences, Inc. (3.19%) | Medtronic Plc (3.02%) | Incyte Corp. (3.31%) |

| 9 | Bristol-Myers Squibb Company (2.94%) | GlaxoSmithKline plc (2.56%) | Regeneron Pharmaceuticals Inc. (2.85%) |

| 10 | Allergan plc (2.91%) | AbbVie, Inc. (2.56%) | McKesson Corp. (2.58%) |

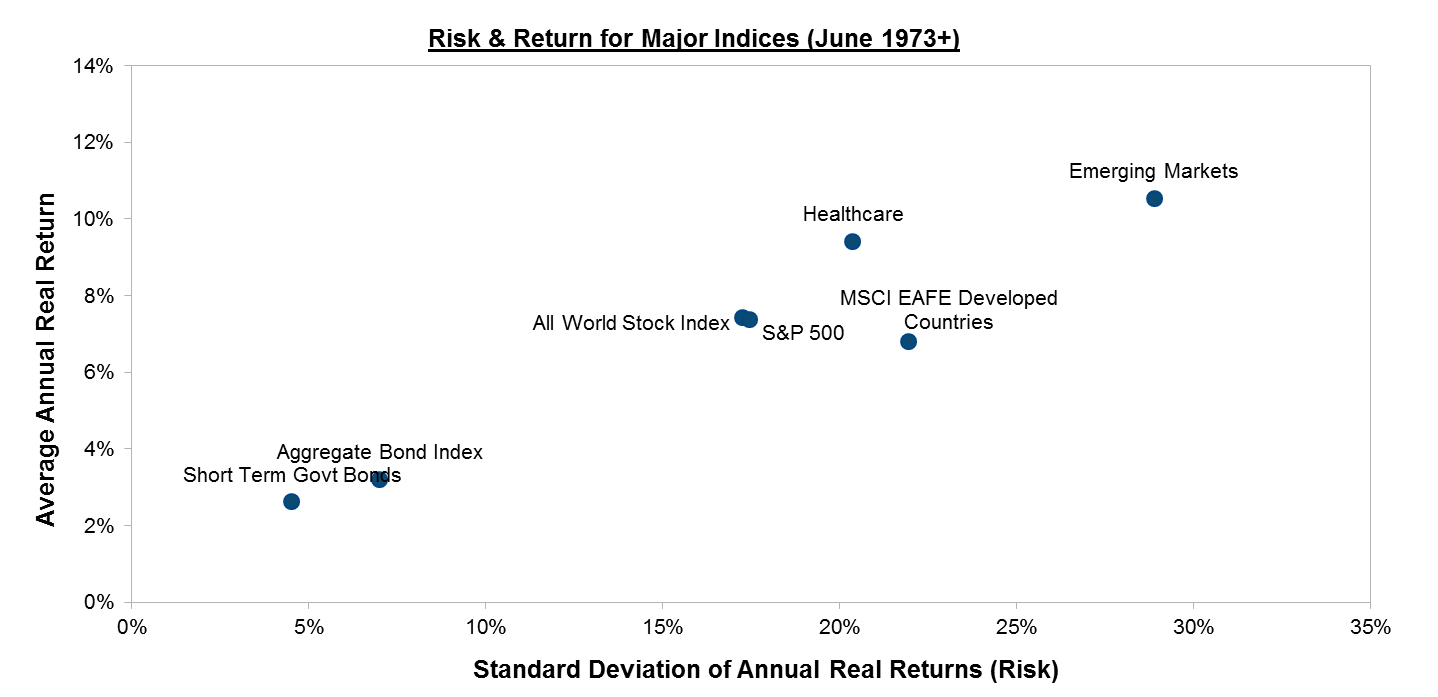

For every sector, we use the relative risk and return profile to determine the size of the positions. We think that, mathematically, there is a correct answer for each decision to allocate your capital to a sector. Many sectors deserve a 0% allocation–or, put another way, they don’t deserve an allocation from you–and a quick way to determine whether a sector is worthwhile is by surveying whether it is historically near the Efficient Frontier.

Healthcare has an attractive ratio of risk and reward relative to other sectors of the global economy. Healthcare has a higher return relative to other assets with a similar amount of volatility. This means it is likely to improve the overall performance of a portfolio with its inclusion.

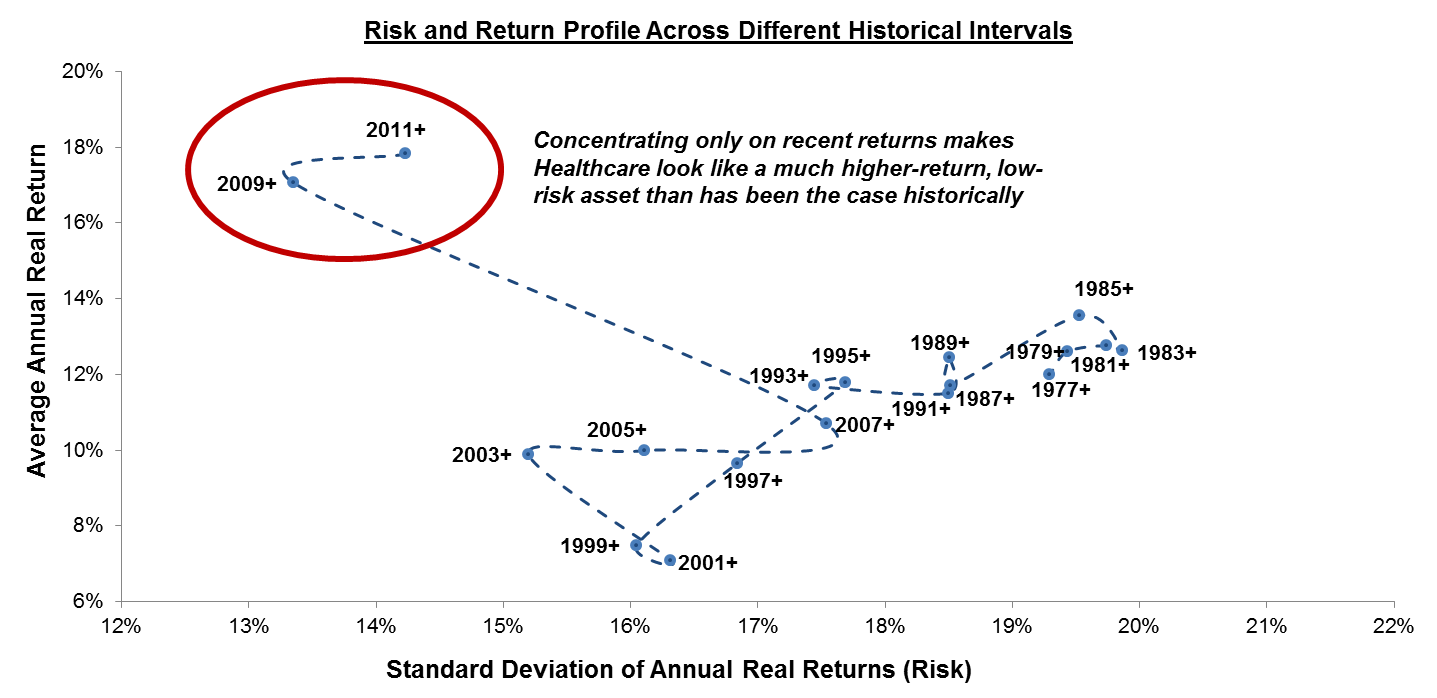

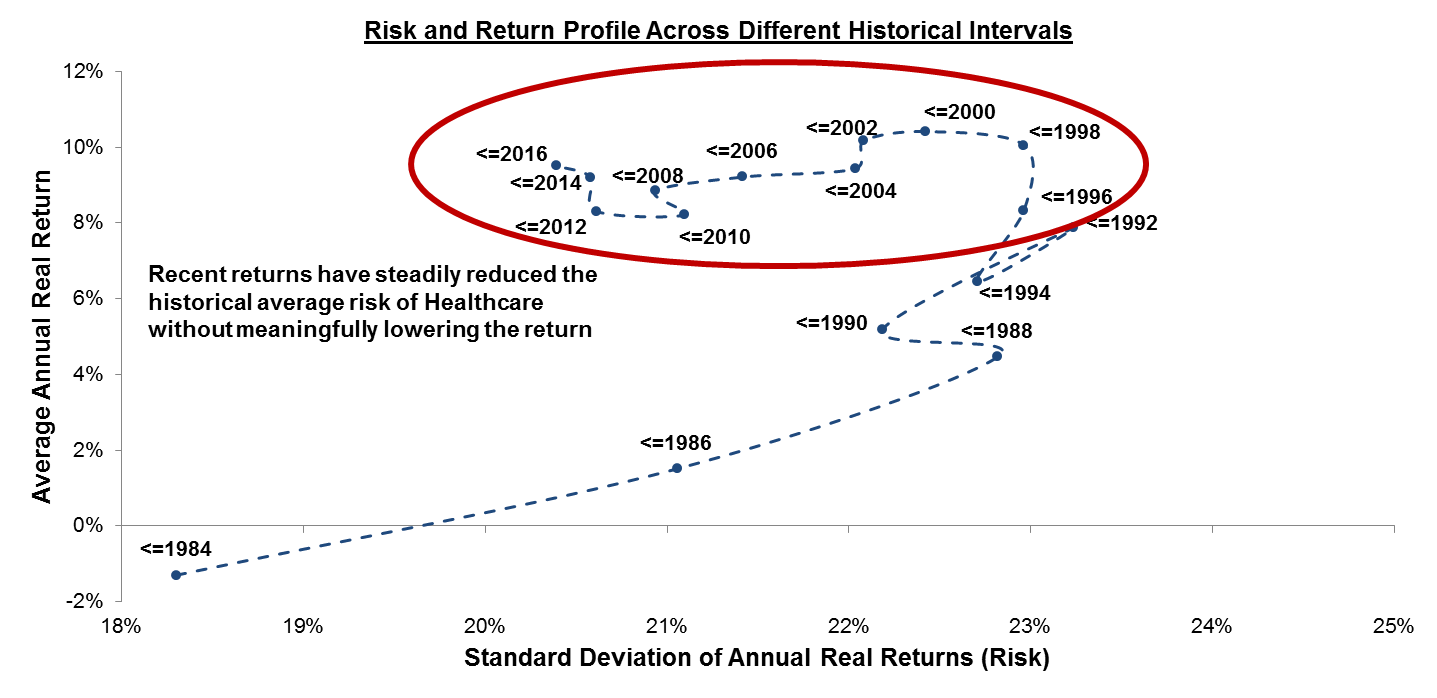

When judging the risk and return of a sector it also matters relative to what time period. Looking only at performance data from 2009 and later means massively overstating the performance of Healthcare relative to it’s historical precedent. You can assume that the performance of the sector from 2009-onward is indicative of the future but that means overruling the entire remaining history of the sector. The net result of the sector’s recent performance has been an apparent decrease in volatility without a decrease in return. The first chart illustrates this effect in the change in the risk-vs-return profile as you move farther back in time, illustrating the danger of only using recent performance data. It’s not until you’ve used at least 15 years of performance data for Healthcare that it begins to profile like its historical precedent.

It’s important to make decisions based not just the historical risk and return of a sector but, as in this case with Healthcare, decisions need to be based on the history of the historical risk and returns. Different Risk and Return assumptions for a sector will result in different optimal allocations. If the recent strong performance in Healthcare does not persist then concentrating only on recent data will influence a decision based on a forecast that was too optimistic.

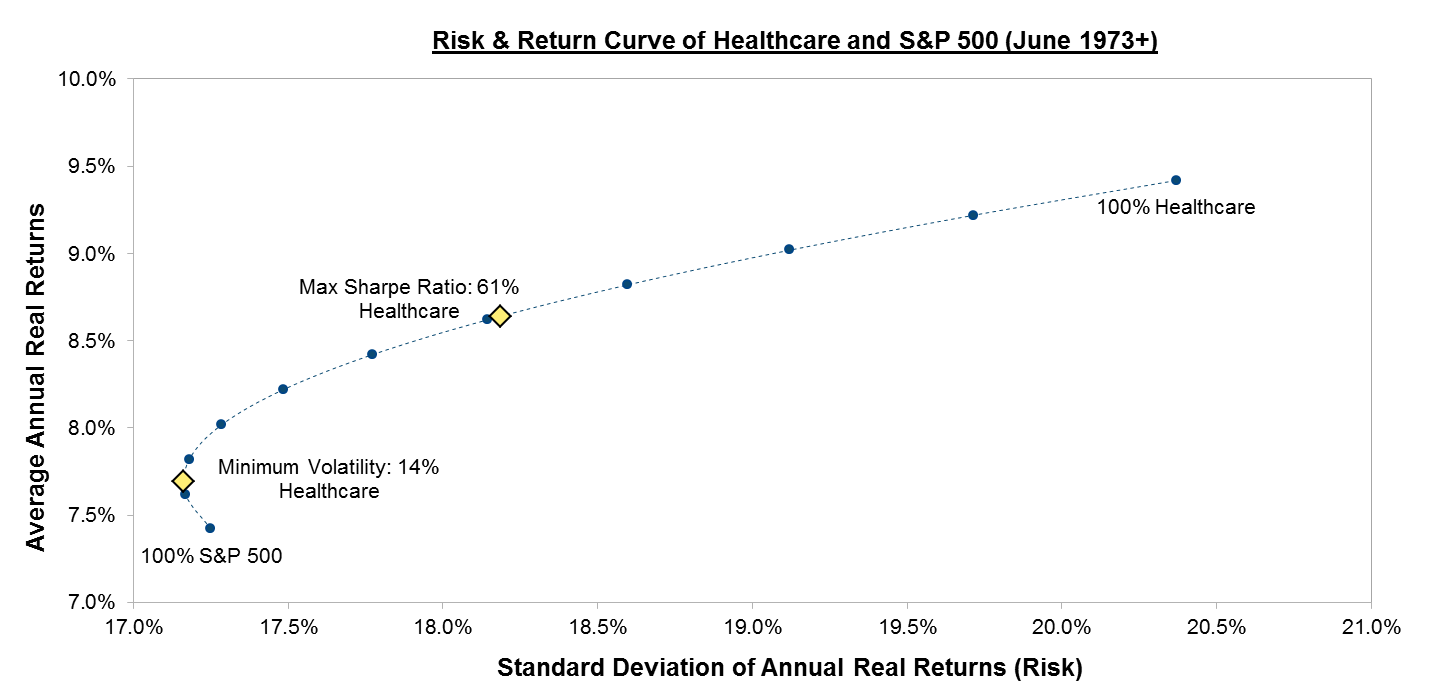

It turns out that Healthcare diversifies most equity indices very effectively, especially the S&P 500. Adding a small allocation to Healthcare has historically boosted returns while also lowering risk.

This pattern continues with other indices as well, suggesting that you can construct a globally diverse portfolio that is better than the sum of its parts by including an additional, overweighted allocation to Healthcare stocks. We’re hopeful that Healthcare will continue its strong performance even in the midst of an ever-changing regulatory environment.

Photo used under Flickr Creative Commons license.

Latest posts from David Loughin

- Healthcare Stocks And Asking “Relative To What?” - November 16, 2016

- The Case for Investing in Energy Companies - October 12, 2016

- Investing In Hong Kong Has Lowered Risk and Boosted Returns - September 28, 2016