Carl Richards, author of The Behavior Gap, has a nice podcast aimed at other financial advisors. Investment News featured one of the podcasts entitled, “How to help clients cope when markets get scary.”

This is Richards’ advice for advisors on what not to do when markets get wild:

During the last few weeks, you’ve probably noticed an uptick in client calls and emails. When the markets start to feel “scary,” people tend to react, even if they have a financial plan. So today, I want to share the story and sketch I use to help people better understand “scary” markets.

Now, I know I’m not the first person to draw a sketch like Fear & Greed. But time after time, it’s been the perfect visual for helping people understand “scary” markets. I like to use the story of what happened in the late ’90s with the technology bubble.

At the top of the market, it seemed like nothing could go wrong, and the money just kept going in to stock mutual funds. In fact, people were setting new records for how much they were investing. But within a matter of months, markets took a serious dip and investors set records for how fast they pulled money out of stock mutual funds. It made zero sense!

The problem with this cycle is that it runs counter to just about every other buying decision we make. We’d never buy a shirt for full price then be O.K. returning it in exchange for the sale price. “Scary” markets convince people this unequal exchange makes sense.

Staying the course when an index investment is down is very uncomfortable in the short-term but usually the best course of action in the long run. Understanding the difference between the two is important.

The short run is anything under five years. That seems like a long period of time to endure falling markets, but when you look at market volatility, it is the best definition. When an index investment is down for three years, the best course of action is probably to rebalance and buy more of it. The more volatile the investment, the more important rebalancing becomes because the rebalancing bonus is dependent upon volatility.

The markets are inherently volatile. We should not be surprised when they move in one direction, up or down, for three years. Historically, that is a very common phenomenon.

The long run begins around 12.5 years. When you look at these longer time periods, on average, you have doubled your money and it will not drop below that level again. After 12.5 years, the average return is even greater than doubling your money, but future volatility means that you may see lower prices at some point in the future.

And of course whenever an index has doubled its value, rebalancing probably means that you should be trimming some of those gains and putting the money into other categories. Rebalancing is the very definition of selling high and buying low.

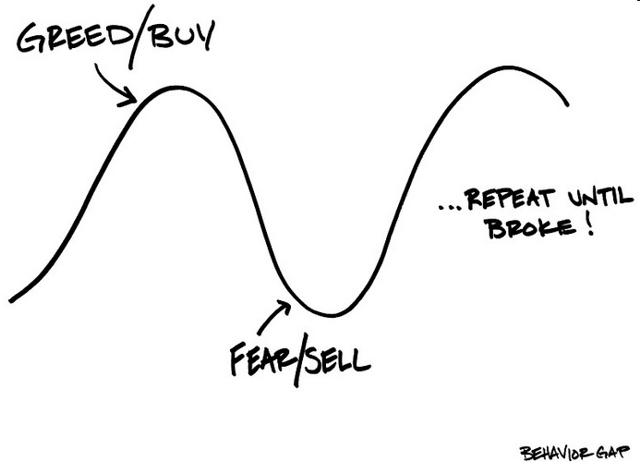

This sage counsel is, of course, contrary to what our emotions would have us do.

Our emotions would have us buy high and sell low as illustrated by Richards’ iconic image accompanying the podcast:

Help your clients to not be taken in by their emotions.

Photo used here under Flickr Creative Commons.

Latest posts from David John Marotta

- #TBT A Review of Finances at Age 60 - July 25, 2024

- #TBT Implement the Automatic Millionaire at Schwab - July 18, 2024

- #TBT Stress Is Not Your Enemy - June 27, 2024