It often doesn’t help to discuss the current state of American personal finances. Successful savers are the minority, but they are the minority you should strive to become. This is a case where following the crowd will hurt you.

However, I read an article recently about the state of personal finances that took a different angle than the average piece.

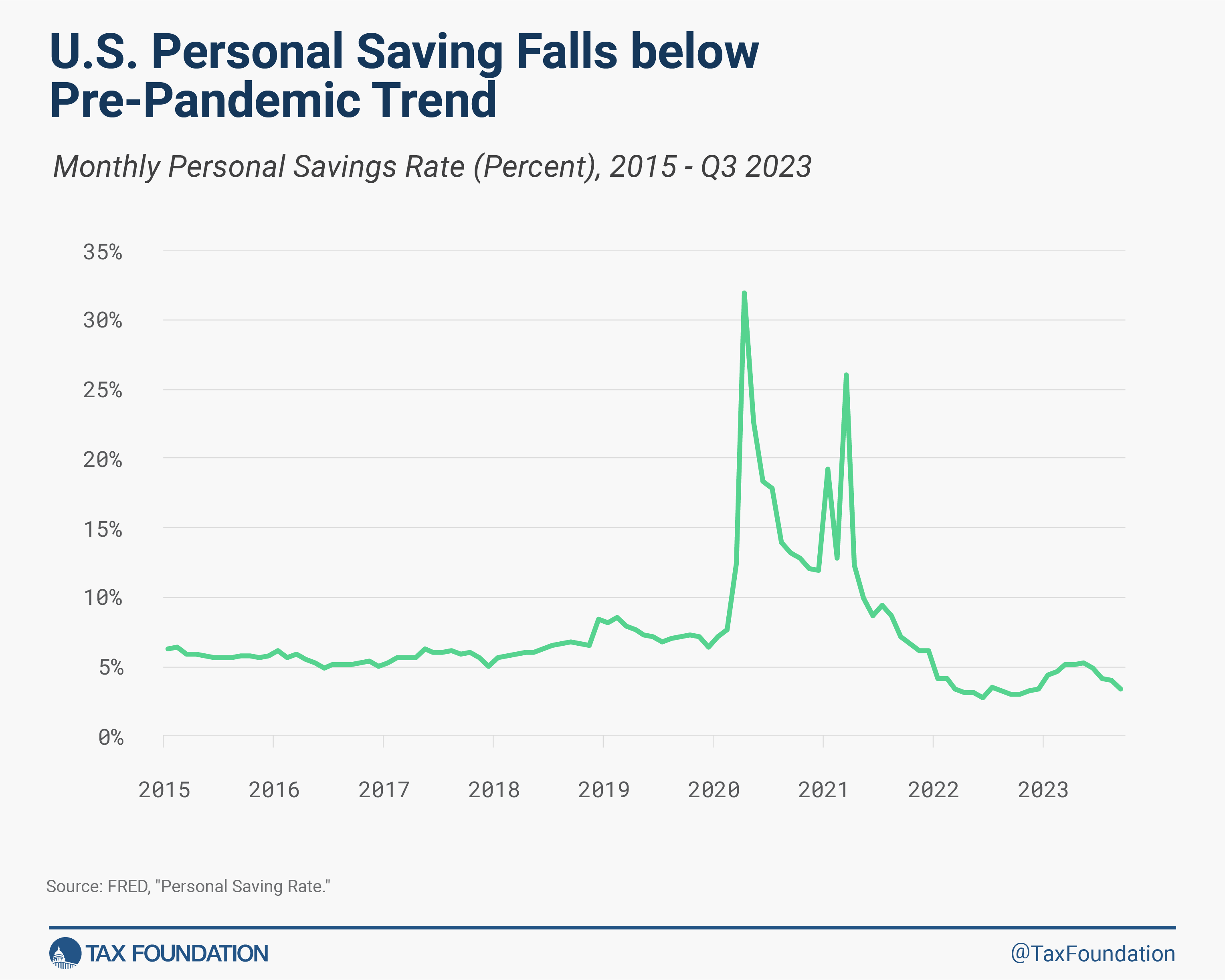

The Tax Foundation authors report that the personal saving rate currently stands at 3.4 percent for September 2023. This is significantly below recommended savings. It is also lower than prepandemic years, as can be seen on their chart:

While this is the sorry state of those who will likely fail to retire, you need not be in that demographic. You can save for retirement even when you are old and broke by either decreasing your lifestyle or pushing back your retirement.

For example, diligent savers can go from broke at age 50 to retiring at age 75 by saving and investing 25.9% of their take home pay annually starting now.

While news stories like this Tax Foundation one normally stop with a story of doom and gloom, the Tax Foundation article goes on to explain how the U.S. tax code is partially to blame for America’s spending problem. They write:

The current federal tax code generally discourages saving , since the income tax applies once to wages and again to the return on wages that are saved.

This is what we are describing in “The Costly Effect Of Saving In A Taxable Account.” In that article, we describe how the 30-year effect of the 1.45% drag of taxation is that you miss out on 256.05% potential future value.

The Tax Foundation authors continue:

By contrast, there is no additional tax on wages that are consumed rather than saved. To make up for this effect, the tax code contains a patchwork of preferences for saving with complicated rules that generally benefit higher-income households (e.g., those who participate in employer-sponsored retirement plans).

Current federal law provides at least 11 different types of tax-preferred saving vehicles, each with a variety of rules and limitations: four main types of retirement saving provisions, three for saving related to education and disabilities, three more for saving related to health and dependent care, and one for saving related to emergencies (a new addition as part of the recently passed Secure 2.0 legislation ).

Other countries have found a simpler solution that is more widely available and useful, boosting savings for households across the income scale. Universal savings accounts (USAs ) are tax-preferred savings vehicles with unrestricted use of funds, allowing participants to save for a variety of reasons including retirement, education, housing, health, unemployment, and emergencies.

The authors go on to discuss how Canada and the United Kingdom both have universal savings accounts with annual contribution limits for after-tax contributions but unlimited tax-free growth and tax-free distributions. In other words, a Roth IRA without the earned income contribution requirement or the age-discriminating distribution rules.

The Tax Foundation authors end the article by saying that:

While policymakers in Congress have introduced limited USAs , a broader overhaul of the tax treatment of saving may be in order as part of fundamental tax reform. As luck would have it, such an opportunity arises at the end of 2025 when individual provisions of the Tax Cuts and Jobs Act expire. Policymakers should use the opportunity to simplify the tax system and encourage saving with the goal of building financial security for low- and middle-income households.

We’re with the Tax Foundation. It is time to scrap the tax code. Anyone of us could design a better system.

Photo by Jackson Simmer on Unsplash. Image has been rotated and radially cropped.

Latest posts from Megan Russell

- Four DPOA Limitations at Schwab and Their Solutions - July 23, 2024

- #TBT Implement the Automatic Millionaire at Schwab - July 18, 2024

- How to Implement a DPOA at Schwab - July 16, 2024