Although most investors and news anchors make this mistake, it is best not to think of the return of the S&P 500 as equivalent to the return of stocks. The S&P 500 represents Large-Cap U.S. stocks which is just half of one asset class.

Although most investors and news anchors make this mistake, it is best not to think of the return of the S&P 500 as equivalent to the return of stocks. The S&P 500 represents Large-Cap U.S. stocks which is just half of one asset class.

In recent years, the S&P 500 has appreciated more than other stock categories. In 2019, the S&P 500 index was up 31.49% for the year. At other times, the S&P 500 has under performed those same stock categories.

Investors always want to compare the return of their portfolio against some benchmark index. We suggest not using the S&P 500 for that purpose. Many years it is not even a good benchmark for the U.S. stock asset class because it represents just one U.S. stock sector.

The most accurate way to determine the measurements of “the stock market” is to measure the return of all stocks in the world, large and small, developed countries and emerging markets, in exactly the proportions that they are valued in the world. The MSCI All Country World Index does just that.

Any decision to deviate from investing like this index is a choice. Tilting small or value is a choice and this year that choice under performed large and growth. The MSCI All Country World Index is a good benchmark against which to compare those choices.

In 2019, the MSCI All Country World Index had a return of 26.60%. This is a good benchmark to use against your stock performance.

However, most portfolios are comprised of both stocks and bonds. Bonds are in a portfolio for stability rather than appreciation. We would expect bonds to dampen returns and protect a portfolio from excess volatility.

In our article “Your Asset Allocation Should Be Priceless,” we demonstrated the importance of having a bond allocation appropriate to your withdrawal rate in order to maximize the chance of not running out of money during your retirement.

Not all bonds are equal. Some bond portfolios are comprised of relatively safe bonds. Other portfolios have a much higher percentage of bonds yet those bonds are comprised of high yield junk bonds that risk acting more like stocks.

We recommend that you aggregate any high yield bond funds with your stock allocation and compare them against a stock index.

If your portfolio includes more secure bonds, you shouldn’t compare your portfolio’s returns against an all-stock index. Instead, you should blend an index which includes a very stable fixed-income portfolio such as the One-Month Treasury Bills index.

Decisions to take significantly more risk with your bonds should not be judged against this type of stable index. You invest in fixed-income because you want stability. You will need that money in the next several years and if you wanted to take risk, you would have invested it in stocks, not bonds.

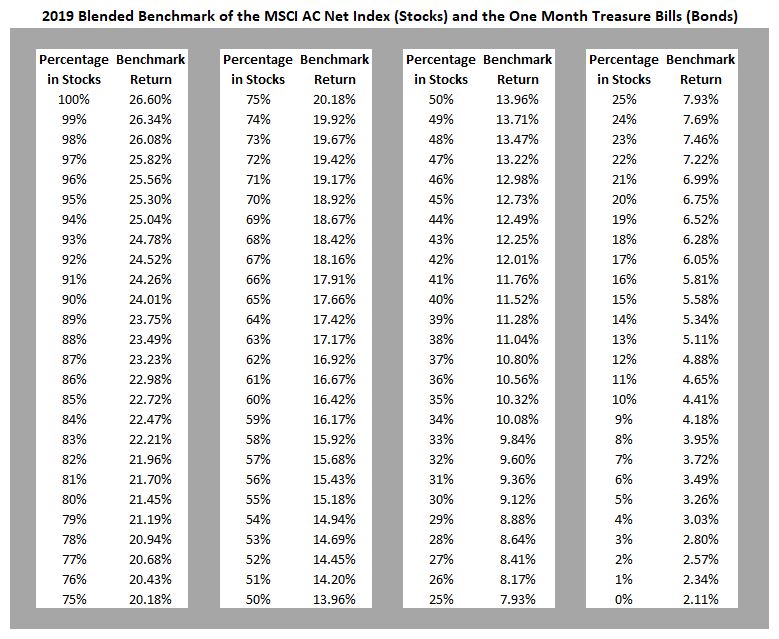

I’ve made a table of that blended index below.

To find the benchmark you should use for your portfolio, determine the percentage of your assets you have invested in stocks and high-yield bonds, and assuming that the remainder of your portfolio is in cash or bonds or other relatively safe fixed-income, use the following table to look up the 2019 blended index where the stock percentage is represented by the MSCI All Country World Index and the bond index is represented by the One-Month Treasury Bills index.

For example, if your portfolio is 70% stocks and 30% bonds and cash, your 2019 blended benchmark return would be 18.92%.

This table computes a blended index comprised of the 2019 monthly returns of the MSCI AC Net Index and the One-Month Treasury Bills index rebalanced monthly for every month of 2019.

Photo by duong chung on Unsplash

Latest posts from David John Marotta

- #TBT A Review of Finances at Age 60 - July 25, 2024

- #TBT Implement the Automatic Millionaire at Schwab - July 18, 2024

- #TBT Stress Is Not Your Enemy - June 27, 2024