Some think the alternative to the traditional insurance providers is the health care sharing ministries, but alas, these programs aren’t insurance.

Health insurance, like all insurance, is no fun to own. In the best case scenario, you have no event and insurance is just losing money. In the worst case, you have an event happen and wish you had insurance to help. There’s no good outcome.

In the health insurance industry, there are two mindsets with a blend in between: first-dollar relief and catastrophic insurance.

First-dollar relief is the idea that healthcare is so important that each person should be able to acquire healthcare without having to pay for it. Some people call this a “right to healthcare,” others just don’t want the threat of a medical bill to make their health decisions for them. It is unpleasant (if not depressing) to do cost-benefit analysis on things as important as medical treatment (ie. How much is 20/20 vision worth to you?). So in first-dollar relief, insurance is used to make all or most medical care free or cheap immediately at the first dollar spent.

In contrast, catastrophic insurance treats medical expenses are like any other day-to-day expense. You do cost-benefit analysis and pay out-of-pocket. Then, insurance is there to protect you from an unseen, costly medical event.

Unlike other insurances, catastrophic health insurance is better thought about as “wealth insurance.” If you were to get catastrophically sick, you would be willing to spend everything and go bankrupt to solve the problem, because if you didn’t then you might not make it to enjoy your savings anyway. Whereas if your house was catastrophically damaged, you might just move on.

Being in good health, not smoking, and not abusing alcohol or drugs, I would lean toward covering your own day-to-day medical expenses out of pocket and having a very high deductible catastrophic health insurance in case of an emergency (and a Health Savings Account for regular expenses, if you have an eligible plan) over having first-dollar relief.

The problem with so-called health ministries is that they are first-dollar relief not catastrophic insurance coverage. Many will cover the most basic things — vitamins prescribed by your doctor, for example — but when it comes to real medical emergencies, they actually have no guarantee that they will cover you, and you have no real legal or financial protection.

So, it only provides relief and no real insurance, which is a bad deal.

Here are the two biggest health ministries in their own words.

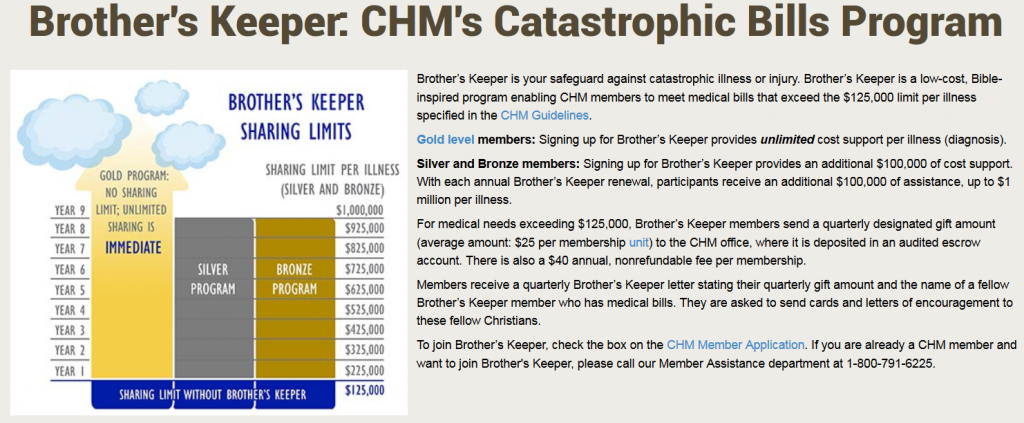

| Christian Healthcare Ministries (CHM)

$125,000 limit per illness The limit can be expanded by paying more money for longer. |

|

| Samaritan Ministries

$250,000 maximum per illness |

|

All of the plans suffer under the burden of first-dollar relief, and most of the plans limit the catastrophic coverage to $250,000.

Only the CHM Brother’s Keeper Gold plan offers something that sounds like wealth protection by aiming to cover unlimited costs, although even this intention is not a legal obligation.

These plans don’t protect your wealth. They don’t protect you from large scale catastrophes. You would be better off saving your money to help cover a traditional deductible and your retirement.

Latest posts from Megan Russell

- Four DPOA Limitations at Schwab and Their Solutions - July 23, 2024

- #TBT Implement the Automatic Millionaire at Schwab - July 18, 2024

- How to Implement a DPOA at Schwab - July 16, 2024