It is the season of spring cleaning, so here’s a calendar of ways to clean up your finances one step at a time. Below I’m starting with this month so you can get started, but in the graphic at right I list them in calendar order.

It is the season of spring cleaning, so here’s a calendar of ways to clean up your finances one step at a time. Below I’m starting with this month so you can get started, but in the graphic at right I list them in calendar order.

April

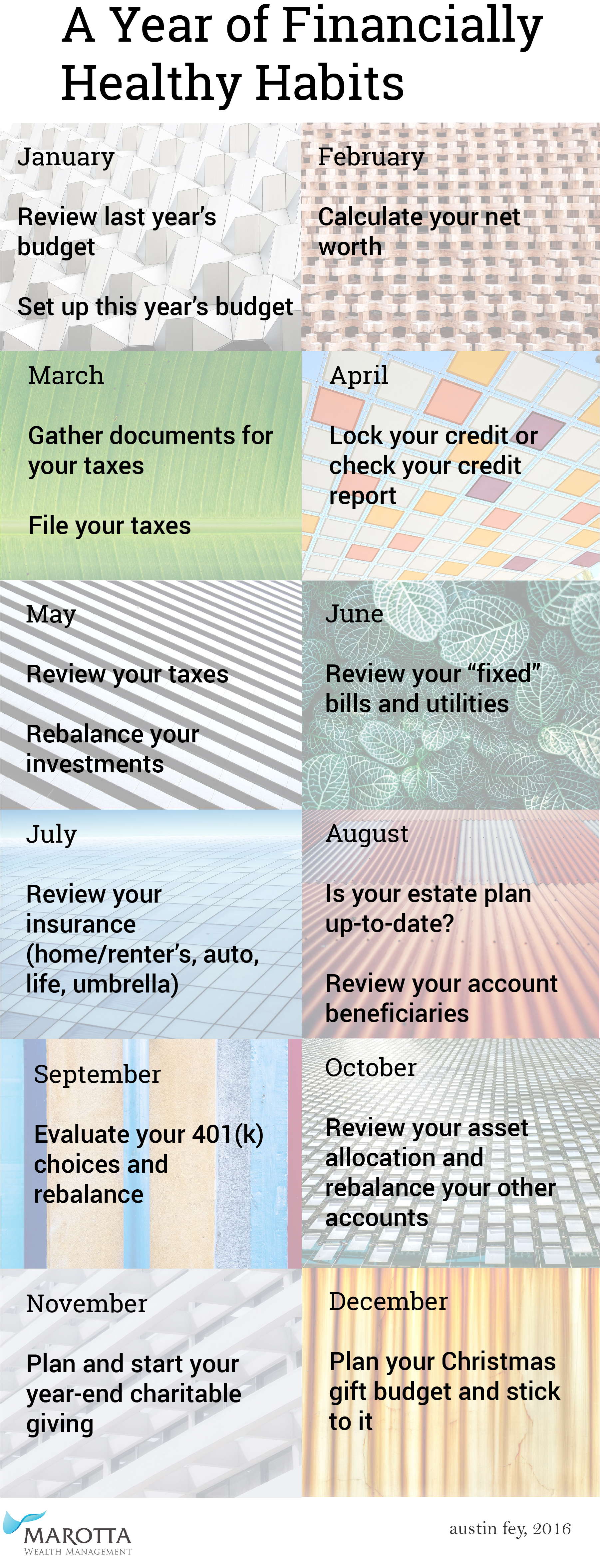

Check your credit report. You could space this out and check one of the three credit bureaus every four months to keep on top of your credit (get a free credit report from TransUnion this month). But at minimum, you should check on your credit once a year. Or better yet, lock your credit down this month, knowing that you can temporarily release the freeze if needed.

May

Review your taxes. No one wants to think about taxes once they’re finished paying, but looking through your taxes is a good exercise. It can help you know how much room you have to realize capital gains, help you calculate how much you’re saving, etc.

June

Review your “fixed” bills and utilities. You may think that you have no control over how much it costs for basic utilities, but this is only partially true. You do not set prices for water and electricity usage, but you control how much you use.

Some other services, such as internet, cable, and phone are actually slightly flexible if you are willing to call their customer service and haggle, or switch to another provider (or threaten to switch).

July

Review your insurance. Do you have home, auto, and umbrella insurance? How is your health insurance and term life insurance?

August

Review your estate plan and make sure it is up-to-date. We suggest revisiting your estate plan every 5-7 years or when you have a major life change.

Review your account beneficiaries to make sure they are in line with your estate plan. There’s nothing worse than having a great estate plan and not following through with the execution.

If you’re spacing out checking your credit, it’s time to get your free report from Equifax.

September

Evaluate your 401(k) choices and rebalance that account. Does the plan allow new money to be invested according to the targets you set up? If so, choosing this option will make it easier to stay close to your target allocation.

Does your employer have a Roth option? This would be a great time to switch to that.

October

Review your other investment asset allocations and rebalance your accounts. You’ve taken care of your 401(k), but now it’s time to take a look at your other investments and rebalance back to your target.

November

Plan your year-end charitable giving, and work with those charities to give a little earlier than most people. Toward the end of the year, charities can be swamped. Giving a little early means you won’t be worried about your gift being processed in the correct calendar year.

December

Plan your Christmas gift budget and stick to it. No one wants to spend their New Year wondering how to pay the bills, so making a budget ahead of time for gifts means you won’t be surprised by the credit card statement. Be strategic about your gift-giving.

If you’re spacing out checking your credit, it’s time to get your free report from Experian.

January

Review last year’s budget. Once you’ve closed the books on the previous year, take some time to see how you did. Where did you spend your money? Evaluate how your spending and saving stacks up with your goals.

Once you’ve looked at last year, it’s time to set up this year’s budget. You might be able to copy some categories over and you might want to adjust others based on your goals, values, and spending habits.

See if you can save even a little bit more each month.

February

Calculate your net worth. Last month you set a budget, and while you should review that every month to see how you’re doing and make adjustments as needed, February is a good time to look at the big picture.

Write down every asset you own and every liability. Subtract liabilities from assets, and that is your net worth. Take some time to brainstorm to remember all the accounts and assets you might own.

March

Gather documents for your taxes. Your employer should have already sent your W-2, and hopefully your other accounts have already sent you tax documents. Send these documents off to your tax preparer, or sit down and file your taxes yourself. Gathering the documents is most of the work!

Calendar Photos used under Unsplash Creative Commons Zero license.

Featured Photo used under Flickr Creative Commons license.

Latest posts from Austin Fey

- 2024 Tax Facts - November 13, 2023

- #TBT Harvest Major Capital Losses Whenever You Have Them - October 26, 2023

- #TBT Testamentary Donor Advised Funds - August 24, 2023