Roth IRA Conversions and Roth Segregation Strategies

on May 29, 2014

with No Comments

Roth accounts have several advantages over traditional retirement accounts.

Roth accounts have several advantages over traditional retirement accounts.

Who would have thought that someone earning $10,700 might want to purposefully push their taxable income up to $217,450 this year in order to pay $47,595 more in taxes at these lower 2012 tax rates?

Who would have thought that someone in the 33% tax bracket now who will be in a lower 28% tax bracket in the future might want to do a Roth conversion at his higher rates now?

Who would have thought that someone earning $400,000 might want to purposefully push their taxable income up to $1.2M this year in order to pay $280,000 more in taxes at these lower 2012 tax rates?

Who would have thought that someone earning $75,000 might want to purposefully push their taxable income up to $275,000 this year in order to pay as much as possible at these lower 2012 tax rates!

You may be a good candidate for a Roth conversion in 2012 if you can answer “yes” to any of these statements.

You can either pay now or pay more later.

While an excess or failed backdoor Roth can feel very stressful to solve, it is a normal and quick fix for your qualified financial custodian.

This new rule says that the account owner can distribute funds from a 529 plan directly to the designated beneficiary’s Roth IRA and have the rollover “be treated in the same manner as the earnings and contributions of a Roth IRA” (meaning no taxation).

Here are three common Roth transactions and how they interact with MAGI for Roth IRA purposes.

For those who run a retirement plan, the next step for implementing this change is to email your plan provider.

For those over age 59 1/2, you would need to withdraw all funds attributable to basis before your withdrawal would be sourced from Roth IRA earnings and the age of your Roth IRA would matter for taxation.

There are several distribution rules that make Roth IRAs great savings tools for early retirees.

Doing some conversion is usually much better than doing no conversion at all. We offer these four simple but effective strategies to calculate a good-enough conversion target for this year.

To take advantage of tax-free penalty-free Roth withdrawals of contribution basis, you need to keep careful records of your Roth contributions.

Fortunately, closing a specific account doesn’t reset your Roth clock.

Roth conversions can only be performed during the IRA owner’s lifetime.

Taxpayers of any income level, age, and employment or retirement status can convert their pre-tax individual retirement assets to Roth IRA.

Once you know how to file it, it is a simple and easy process.

What can you do when you are in the middle of the Roth IRA contribution phaseout range?

Nothing changes during a Bear Market when it comes to where you should save and invest.

If you have an accepting employer plan, you could consider rolling the pre-tax funds into your 401(k) this year while converting your nondeductible basis cleanly to a Roth IRA.

This person has an IRA balance, but is about to empty it with a reverse Rollover. So the question is one of timing: can they do the IRA Rollover before the nondeductible contribution so that their cream and coffee never mix?

Having a 401(k) plan with both pre- and post-tax balances is quite common, but mistakes are common as well.

This person has no IRA balance, but is about to get one with an IRA Rollover. So the question is one of timing: can they do the IRA Rollover after the nondeductible contribution has already been converted so that their cream and coffee never mix?

These are two simple but effective strategies to help calculate a very good conversion target for this year.

Under the Tax Cuts and Jobs Act, you are still allowed to make nondeductible contributions and still allowed to convert IRA assets to Roth IRA.

On January 18, 2018, the IRS updated their Frequently Asked Questions page to come into line with the new Tax Cuts and Jobs Act.

Seriously, open and fund your Roth IRA now. You’ll regret it later if you don’t get started now.

It is an inconvenience during the holiday season to say the least, but Roth conversions are worth the effort.

Like how diner coffee gets more bitter as the waitress tops off your cup with more coffee from the pot, so too the growth on your nondeductible assets increases your tax owed by decreasing the percent post-tax assets in your cup.

Yikes! This is a costly mistake.

You can’t touch the earnings on your contributions until you’ve had an account open for 5 years and you’re either over age 59 ½ or you meet special exceptions.

Taking the smallest distribution each year will ensure the beneficiary achieves the maximum tax-free growth of tax-free income.

A Roth recharacterization is a true undo; it is as though you never converted those assets in the eyes of the IRS. This includes recalculating your RMD had you not converted the assets.

Annual required minimum distributions must be satisfied before any additional amounts are converted to a Roth IRA.

I’m on the borderline for being able to contribute to a Roth IRA. How do I determine how much I can contribute?

Regardless of the reason, if you have put too much money in your Roth IRA, the solution is the same.

Even over the income threshold, you may still be able to add funds to your Roth IRA with what is called a backdoor Roth.

Most tax professionals don’t think of such tax planning opportunities, because they have to focus on complying with tax accounting regulations.

Sometimes, there isn’t enough to do it all. Even then, fund your Roth.

A complete guide to using Roth IRAs to build lasting wealth.

A backdoor Roth IRA contribution requires some extra steps but allows high-income earners equal access to the tax-free benefits of a Roth IRA.

Mr. Roth can also help with transferring gifts to your heirs, setting up your first emergency reserve account, and paying for a new house or college expenses. But don’t ask him to iron your clothes. That’s where he draws a line.

There is a backdoor way to contribute to a Roth IRA for those who are not income eligible. This method requires the following steps:

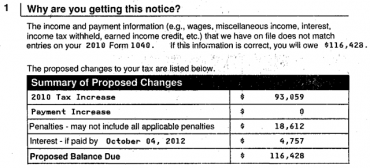

Currently the IRS is sending notices to anyone who did a Roth Recharacterization in 2010 asking them to pay as though they kept the entire conversion amount.

David John Marotta was featured in a Wall Street Journal article about the upcoming Roth recharacterization deadline.

Marotta’s Roth segregation technique of conversion and recharacterization was featured in InvestmentNews magazine.

If you failed to convert anything last year, you missed an opportunity. If you converted much more than you probably wanted to, now you have to decide how much to keep.