Safeguard #7: Avoid Investment Advisors Who Sugarcoat Reality

on June 22, 2009

with No Comments

Excellent advisors communicate clearly exactly how bad the markets have been and can be.

David John Marotta and Megan Russell co-author a syndicated financial column featured in several newspapers across the country.

Excellent advisors communicate clearly exactly how bad the markets have been and can be.

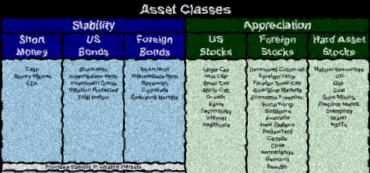

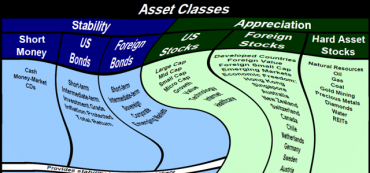

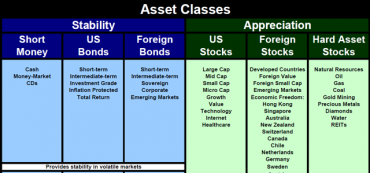

Rebalancing between asset classes boosts returns and decreases volatility. But setting your asset classes based on sectors of the economy is not an effective strategy.

In this formula is deep wisdom, both for portfolio construction and for determining which categories are worth regular rebalancing.

Generally, a correlation that can drop below 0.6 with other asset classes is a good candidate to become its own asset class.

Diversifying your portfolio means finding assets that have value on their own merits but do not move exactly alike. A critical investment metric called “correlation” is used to construct a portfolio most likely to meet your personal financial goals.

Estate planning must begin with family harmony as the goal. Thus personal dynamics are more important than avoiding probate and estate taxes.

The most important product of estate planning is achieving family harmony. Think carefully when you choose your executor or trustee.

There isn’t a better time to invest than today. Getting started can be intimidating, but these simple steps will help you through your first few years of investing.

The various congressional bailouts have been touted as essential to the nation’s economic security. So long as the notion of economic security remains vague and abstract, it has wide support. But anyone who examines the details should realize this so-called security threatens our freedom and stability.

To safeguard your money, you must be able to extricate yourself from any bad investment quickly. Of course, the companies that sell mistakes don’t want you to be able to do that, so they use financial hooks to hold your money captive.

You have a critical part to play in financial planning. Certain responsibilities cannot be delegated to others.

Crazy volatile markets push people toward irrational investment schemes. Know how to avoid them in order to safeguard your money.

One important safeguard is to insist on investing only in liquid assets. Investors undervalue liquidity 99.9% of the time. You need to be in the other 0.1%.

There are several investment safeguards you should insist on. One is to avoid any investment opportunity that sounds too good to be true.

I was recently asked if investors should trust their financial advisors. And my short answer, you may be surprised to hear, was no. Your financial advisor should not also have custody of your investments.

Christians celebrate the birth of Jesus on Christmas Day. But for too many of us, it’s the season that unravels the careful financial planning of the previous 11 months. So this year, instead of trading your financial goals for a mountain of gifts and debt, take a moment to contemplate how a spiritual perspective can help you put your wealth in perspective.

Philip Zimbardo’s latest book, “The Time Paradox” suggests that understanding your own time perspective may help you unlock the secrets of financial freedom. In other words, how we think determines who we are and what we do.

How you “title” the property you own is a lot more important than you might think. Failure to title your assets properly could undo the best will and trust planning that money can buy.

Free markets are under assault in America. We have seen much hyperbole and slander in these past two years of political polarization. But the idea of capitalism and free markets has received more negative campaigning and vicious attack than both candidates combined.

All this toil to maintain an average benefit of about $12,000 a year!

When a hurricane threatens, making a plan and gearing up for emergencies is imperative. Economic emergencies happen too, but it may be less obvious how to prepare. Here are seven steps you should take to weather any financial storm.

Regulation and centralized planning have caused financial instability and failing institutions. If this is the root cause, then many of the proposed solutions will only make matters worse.

To process financial information, our minds often attempt unwise shortcuts. By understanding behavioral finance, we can limit the information we use and keep our decisions balanced and on track.

One of the early studies on herd mentality was the Solomon Asch experiments in the 1950s. The setup was a mock vision test. In reality, all but one of the participants were actors, who after a few correct answers started agreeing unanimously on a wrong choice.

Think of confidence as a continuum: Lack of confidence is paralyzing, self-confidence is good, but overconfidence is deadly. Successful investors seek to find a balance between rashness and timidity. Understanding the psychology that causes us to act overconfidently will help you avoid it.

The essence of successful financial planning is using your money to meet your life’s goals. Curiously our minds tend to fall prey to the fallacy that behavioral finance calls “mental accounting”.

Our first reaction to a complicated situation, usually instinctive, often does not serve our best interests. One heuristic that the brain uses to solve complex evaluations is to make an initial guess and then adjust from that point. This mental process is called “anchoring.”

You can both diversify for safety and boost your returns by adding international investments to your portfolio.

A year ago when the markets were all setting new highs, people were asking what they should do with their retirement portfolio. I answered, “Rebalance.” Now that the market is setting new lows, I get the same question, and my response hasn’t changed.

You can hedge your assets against underreported inflation and protect your retirement goals.

Inflation at this rate causes serious harm to our nation’s economy and its citizens.

Officially, inflation today is calculated about 4%. Unofficially, it is over 7%.

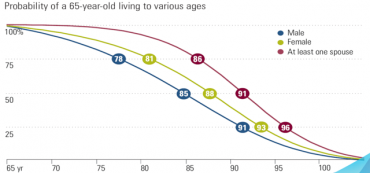

Certain assumptions such as maximum safe withdrawal rate are critical in order not to compromise a long and successful retirement.

The subprime mortgage meltdown has cost the world 15% of its market capitalization, about $9 trillion. The primary culprit who caused all of this financial loss, pain and suffering is not the mortgage companies.

It used to be that becoming a millionaire was regarded as a huge achievement. In today’s dollars, however, it is fairly trivial. The new rich is over $5 million.

Investors are fickle. Investing should not be. When your investments go down, even slightly, you may be tempted to make poor choices.

Gold may glitter, but it is still better to own the mine.

Psychologists suggest we feel a loss about 2.5 times as much as an equivalent gain. Even with a brilliant investment plan, it takes diligence to overcome our emotional biases and avoid making investing mistakes.

Here we offer some sound advice on how to put the money you’ve saved to work for you.

If you’re like most of today’s college graduates, you may find yourself ill prepared for the real world of financial responsibility. You never saw how your parents lived when they were first married and struggling. Consequently, you may be basing your after-school expectations on an upper-middle-class lifestyle. Here is my financial advice for those of you learning to live on your own.

You owe it to yourself and your family to make certain you keep your financial New Year’s resolutions this year.

You can use both investment losses and investment gains to good tax advantage.

Below the line deductions are uncertain. Like many items in the tax code the correct answer to “Will they reduce my taxes?” is: “It depends.”

As Glinda advises us, “It’s always best to start at the beginning,” and at the beginning of the tax return is determining your filing status.

Most Americans look backward and only hope that Uncle Sam will return some of what they have already paid, but those with wealth look ahead and adjust their affairs according to the tax code.

Last week we listed the ways university student are enticed into using credit cards. This week we will examine the economical impact of those initially small and convenient monthly payments.

Although 60% of college student’s pay off their balance each month, that leaves 40% who do not.

Most people want to honor their debt. But many families have allowed their debt to spiral out of control, and they feel helpless, ashamed, and at a loss to know what to do. While bankruptcy isn’t anyone’s first choice, sometimes it is an important choice to consider.

Those actually seeing the movie in a theater provide only 14% of a film’s revenue.

One of the asset classes that we use to build diversified portfolios consists of hard asset stocks.